Macroprudential policy measures

Published as part of the Macroprudential Bulletin 5, April 2018.

This document provides an overview of the macroprudential policy measures that are being implemented in euro area countries as of 1 April 2018. An overview of all measures reported to the ECB under Article 5 of the SSM Regulation[1] is provided on the ECB’s website.[2]The macroprudential policy measures are defined in the ECB’s web glossary for macroprudential policy and financial stability. Their aim is described in further detail in the first issue of the Macroprudential Bulletin.

1 Macroprudential policy measures – an overview

The table below provides an overview of macroprudential policy measures in the euro area on 1 April 2018.

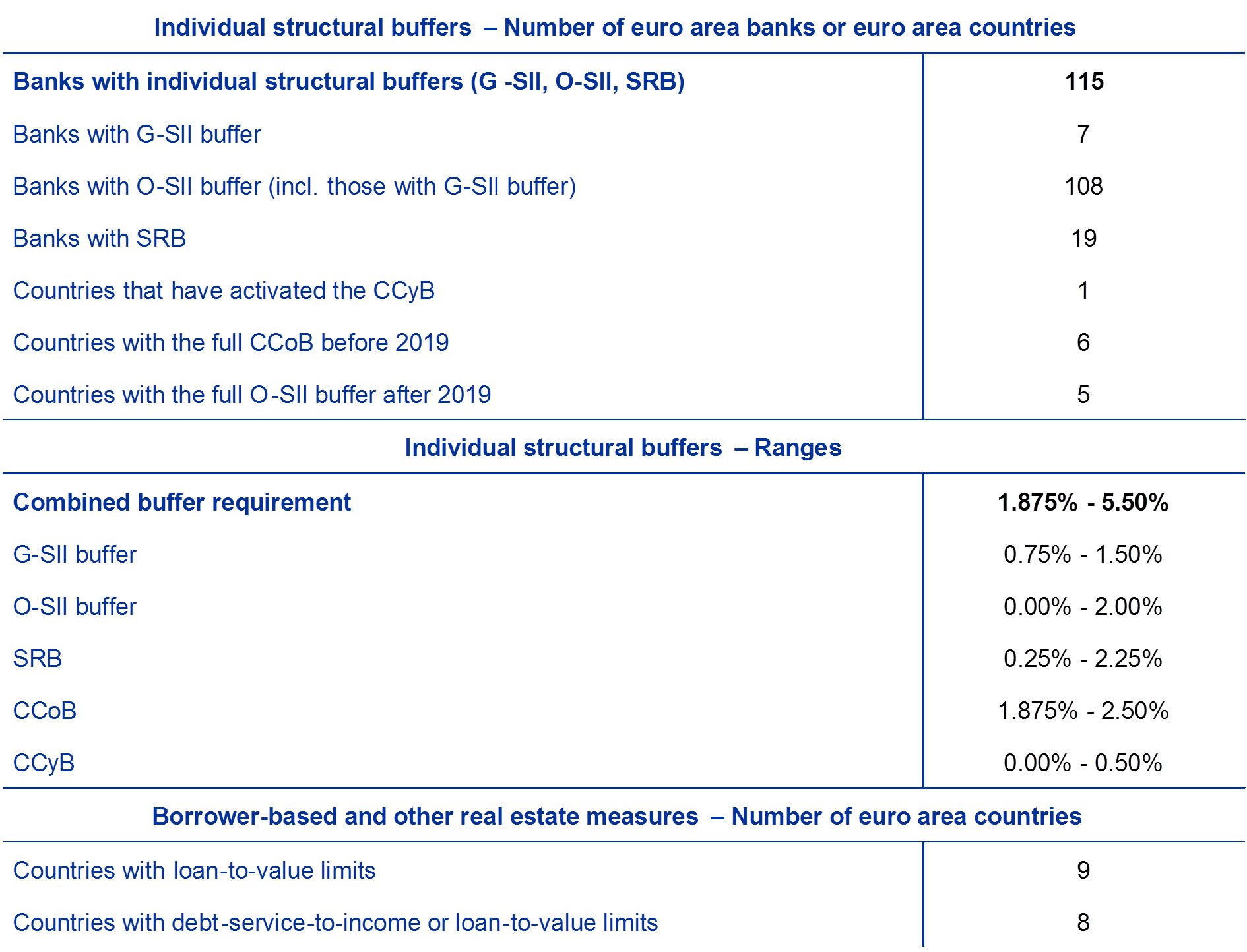

Table 1

Macroprudential policy measures

(as of 1 April 2018)

Source: National notifications.

Notes: The figures only include information on supervised banks (e.g. excluding O-SII buffer requirements for Cyprus investment firms). Small and medium-sized investment firms are exempted from the CCyB and/or the CCoB in Italy, Lithuania, Luxembourg, Malta and Slovakia. For Estonia and Slovakia, the SRB is applied only to domestic exposures, meaning that the buffer applies in addition to the O-SII or G-SII buffer, whichever is greater. For Estonia, the SRB is applied to all banks. In Ireland and Portugal, the full O-SII buffer will be implemented in 2021; in Cyprus, Greece and Italy in 2022. The acronyms used in the above table and notes are as follows: global systemically important institution (G-SII); other systemically important institution (O-SII); systemic risk buffer (SRB); countercyclical capital buffer (CCyB); and capital conservation buffer (CCoB).

2 Capital requirements at the country level

Figure 1 shows the minimum and the maximum combined buffer requirements (CBRs), as well as the banks affected by the maximum CBR. Whereas the minimum CBR (blue) is usually applicable to all banks in one country, taking into account the capital conservation buffer (CCoB) and the countercyclical capital buffer (CCyB), the maximum CBR (yellow) relates to financial institutions that are required to apply the other systemically important institution (O-SII), global systemically important institution (G-SII) or systemic risk buffer (SRB), whichever is greater.[3]

Figure 1

Overview of combined buffer requirements

(left-hand scale: percentage of total risk exposure; right-hand scale: total number)

Source: National notifications.

Notes: In some countries, certain financial institutions are designated O-SIIs, but no additional buffer requirement applies at this time. Small and medium-sized investment firms are exempted from the CCyB and/or the CCoB in Italy, Lithuania, Luxembourg, Malta and Slovakia. For Estonia and Slovakia, the SRB is applied only to domestic exposures, meaning that the buffer applies in addition to the O-SII or G-SII buffer, whichever is greater. The figures only include information on supervised banks (e.g. excluding O-SII buffer requirements for CY investment firms). The acronyms used in the above figure and notes are as follows: combined buffer requirement (CBR); global systemically important institution (G-SII); other systemically important institution (O-SII); systemic risk buffer (SRB); countercyclical capital buffer (CCyB); and capital conservation buffer (CCoB).

© European Central Bank, 2018

Postal address 60640 Frankfurt am Main, Germany

Telephone +49 69 1344 0

Website www.ecb.europa.eu

All rights reserved. Reproduction for educational and non-commercial purposes is permitted provided that the source is acknowledged.

ISSN 2467-1770 DOI 10.2866/351597

ISBN 978-92-899-3195-3 EU catalogue No QB-CA-18-001-EN-Q

Cut-off date: 19 April 2018.

In one country (Estonia), the SRB applies to all banks. In Estonia and Slovakia, the SRB is applied only to domestic exposures, meaning that the buffer is in addition to the O-SII or G-SII buffer, whichever is greater.