Economic, financial and monetary developments

Summary

At its meeting on 18 July 2024, the Governing Council decided to keep the three key ECB interest rates unchanged. The incoming information broadly supports the Governing Council’s previous assessment of the medium-term inflation outlook. While some measures of underlying inflation ticked up in May owing to one-off factors, most measures were either stable or edged down in June. In line with expectations, the inflationary impact of high wage growth has been buffered by profits. Monetary policy is keeping financing conditions restrictive. At the same time, domestic price pressures are still high, services inflation is elevated and headline inflation is likely to remain above the target well into next year.

The Governing Council is determined to ensure that inflation returns to its 2% medium-term target in a timely manner. It will keep policy rates sufficiently restrictive for as long as necessary to achieve this aim. The Governing Council will continue to follow a data-dependent and meeting-by-meeting approach to determining the appropriate level and duration of restriction. In particular, its interest rate decisions will be based on its assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation and the strength of monetary policy transmission. The Governing Council is not pre-committing to a particular rate path.

Economic activity

The incoming information indicates that the euro area economy grew in the second quarter, but likely at a slower pace than in the first quarter. Services continue to lead the recovery, while industrial production and goods exports have been weak. Investment indicators point to muted growth in 2024, amid heightened uncertainty. Looking ahead, the recovery is expected to be supported by consumption, driven by the strengthening of real incomes resulting from lower inflation and higher nominal wages. Moreover, exports should pick up alongside a rise in global demand. Finally, monetary policy should exert less of a drag on demand over time.

The labour market remains resilient. The unemployment rate was unchanged, at 6.4% in May, remaining at its lowest level since the start of the euro. Employment, which grew by 0.3% in the first quarter, was supported by a further increase in the labour force, which expanded at the same rate. More jobs are likely to have been created in the second quarter, mainly in the services sector. Firms are gradually reducing their job postings, but from high levels.

National fiscal and structural policies should aim at making the economy more productive and competitive, which would help to raise potential growth and reduce price pressures in the medium term. An effective, speedy and full implementation of the Next Generation EU programme, progress towards capital markets union and the completion of banking union, and a strengthening of the Single Market are key factors that would help foster innovation and increase investment in the green and digital transitions. The Governing Council welcomes the European Commission’s recent guidance calling for EU Member States to strengthen fiscal sustainability and the Eurogroup’s statement on the fiscal stance for the euro area in 2025. Implementing the EU’s revised economic governance framework fully and without delay will help governments bring down budget deficits and debt ratios on a sustained basis.

Inflation

Annual inflation eased to 2.5% in June, from 2.6% in May. Food prices went up by 2.4% in June – which is 0.2 percentage points less than in May – while energy prices remained essentially flat. Both goods price inflation and services price inflation were unchanged in June, at 0.7% and 4.1%, respectively. While some measures of underlying inflation ticked up in May owing to one-off factors, most measures were either stable or edged down in June.

Domestic inflation remains high. Wages are still rising at an elevated rate, making up for the past period of high inflation. Higher nominal wages, alongside weak productivity, have added to unit labour cost growth, although it decelerated somewhat in the first quarter of this year. Owing to the staggered nature of wage adjustments and the large contribution of one-off payments, growth in labour costs will likely remain elevated over the near term. At the same time, recent data on compensation per employee have been in line with expectations and the latest survey indicators signal that wage growth will moderate over the course of next year. Moreover, profits contracted in the first quarter, helping to offset the inflationary effects of higher unit labour costs, and survey evidence suggests that profits should continue to be dampened in the near term.

Inflation is expected to fluctuate around current levels for the rest of the year, partly owing to energy-related base effects. It is then expected to decline towards the target over the second half of next year, owing to weaker growth in labour costs, the effects of the Governing Council’s restrictive monetary policy and the fading impact of the past inflation surge. Measures of longer-term inflation expectations have remained broadly stable, with most standing at around 2%.

Risk assessment

The risks to economic growth are tilted to the downside. A weaker world economy or an escalation in trade tensions between major economies would weigh on euro area growth. Russia’s unjustified war against Ukraine and the tragic conflict in the Middle East are major sources of geopolitical risk. This may result in firms and households becoming less confident about the future and global trade being disrupted. Growth could also be lower if the effects of monetary policy turn out stronger than expected. Growth could be higher if inflation comes down more quickly than expected and rising confidence and real incomes mean that spending increases by more than anticipated, or if the world economy grows more strongly than expected.

Inflation could turn out higher than anticipated if wages or profits increase by more than expected. Upside risks to inflation also stem from the heightened geopolitical tensions, which could push energy prices and freight costs higher in the near term and disrupt global trade. Moreover, extreme weather events, and the unfolding climate crisis more broadly, could drive up food prices. By contrast, inflation may surprise on the downside if monetary policy dampens demand more than expected, or if the economic environment in the rest of the world worsens unexpectedly.

Financial and monetary conditions

The policy rate cut in June has been transmitted smoothly to money market interest rates, while broader financial conditions have been somewhat volatile. Financing costs remain restrictive as the previous policy rate increases continue to work their way through the transmission chain. The average interest rate on new loans to firms edged down to 5.1% in May, while mortgage rates remained unchanged at 3.8%.

Credit standards for loans remain tight. According to the July 2024 bank lending survey, standards for lending to firms tightened slightly in the second quarter, while standards for mortgages eased moderately. Firms’ demand for loans fell slightly, while households’ demand for mortgages rose for the first time since early 2022.

Overall, credit dynamics remain weak. Bank lending to firms and households grew at an annual rate of 0.3% in May, only marginally up from the previous month. The annual growth in broad money – as measured by M3 – rose to 1.6% in May, from 1.3% in April.

Monetary policy decisions

The interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility remain unchanged at 4.25%, 4.50% and 3.75% respectively.

The asset purchase programme portfolio is declining at a measured and predictable pace, as the Eurosystem no longer reinvests the principal payments from maturing securities.

The Eurosystem no longer reinvests all of the principal payments from maturing securities purchased under the pandemic emergency purchase programme (PEPP), reducing the PEPP portfolio by €7.5 billion per month on average. The Governing Council intends to discontinue reinvestments under the PEPP at the end of 2024.

The Governing Council will continue applying flexibility in reinvesting redemptions coming due in the PEPP portfolio, with a view to countering risks to the monetary policy transmission mechanism related to the pandemic.

As banks are repaying the amounts borrowed under the targeted longer-term refinancing operations, the Governing Council will regularly assess how targeted lending operations and their ongoing repayment are contributing to its monetary policy stance.

Conclusion

The Governing Council decided at its meeting on 18 July 2024 to keep the three key ECB interest rates unchanged. The Governing Council is determined to ensure that inflation returns to its 2% medium-term target in a timely manner. It will keep policy rates sufficiently restrictive for as long as necessary to achieve this aim. The Governing Council will continue to follow a data-dependent and meeting-by-meeting approach to determining the appropriate level and duration of restriction. In particular, the interest rate decisions will be based on the Governing Council’s assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation and the strength of monetary policy transmission. The Governing Council is not pre-committing to a particular rate path.

In any case, the Governing Council stands ready to adjust all of its instruments within its mandate to ensure that inflation returns to its medium-term target and to preserve the smooth functioning of monetary policy transmission.

1 External environment

Global economic activity and trade remained on a steady upward trajectory in the second quarter of 2024. Survey data indicate that the global economy is likely entering a period of restocking which should support trade in the period ahead. Inflation continues to moderate, yet pressures on services prices are persistent.

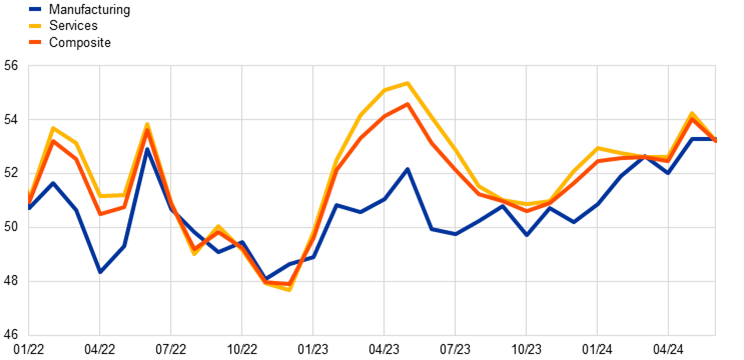

Global activity, excluding the euro area, is still on a steady upward trajectory. The June global composite output Purchasing Managers’ Index (PMI) remained in expansionary territory (Chart 1). The headline index edged down from 54.0 in May to 53.2 in June, closer to its long-term average. This reflects a weakening of services activity at the same time as output in the manufacturing sector stayed unchanged. Services activity moderated across most key economies – including China in particular − while remaining in expansionary territory. The ECB’s global growth nowcasting model confirms that the global expansion is ongoing. While this assessment is mainly underpinned by soft data, most hard data have also become more supportive. Overall, this suggests that global activity growth remained on a steady upward trajectory in the second quarter of 2024.

Chart 1

Global output PMI

(diffusion indices)

Sources: S&P Global Market Intelligence and ECB staff calculations.

Note: The latest observations are for June 2024.

Global trade rebounded at the start of the year and is expected to strengthen further, supported by the recent turn in the inventory cycle. The expected recovery from last year’s weak trade figures was confirmed by hard data, with global import growth amounting to 0.6% quarter on quarter in the first quarter of the year. In the short term, stronger industrial production data point towards a further rebound in trade growth. The recent turn in the global inventory cycle has also boosted trade. In the second half of 2023 growth in inventories fell sharply and even turned negative, suggesting that rising demand was partly met by drawing down stocks. With new orders continuing to increase in 2024, survey data suggest that inventories are being rebuilt. In fact, PMI readings of inventories at the global level have risen more quickly than measures of new orders. This suggests that the global economy may be entering a period of restocking, which could support trade going forward.[1]

Inflation across OECD economies continues to moderate, yet services price pressures are persistent. In May the annual headline rate of consumer price index (CPI) inflation across OECD countries (excluding Türkiye) declined marginally to 2.9%, compared with 3.0% in the previous month (Chart 2). Excluding food and energy prices, OECD core inflation continued to slow, to 3.2% in May, down 0.1 percentage points from April. Falling goods prices and slower increases for other services components are reducing inflationary pressures in advanced economies. However, inflation in labour-intensive activities such as restaurants and hotels, recreation, culture and health care remains elevated and is only moving sluggishly in the direction of average pre-pandemic rates. This suggests that in many countries, wage growth remains high amid tight labour markets. In addition, rent inflation is still elevated and often well above pre-pandemic levels. Looking ahead, headline CPI inflation is only expected to continue falling gradually.

Chart 2

OECD CPI inflation

(year-on-year percentage changes)

Sources: OECD and ECB staff calculations.

Notes: The OECD aggregate excludes Türkiye and is calculated using OECD CPI annual weights. The latest observations are for May 2024.

Since the last Governing Council meeting, Brent crude oil prices have increased by around 11% on the back of expectations of tighter supply and rising geopolitical concerns. Oil prices rebounded substantially after OPEC+ officials clarified that the phasing out of the voluntary cut in production announced at their June meeting would depend on prevailing market conditions, which signalled the possibility of tighter supply conditions than initially expected. Geopolitical tensions, including renewed fears of deepening conflict involving Hezbollah in Lebanon, Ukrainian drone strikes on Russian oil facilities and Houthi attacks on commercial shipping in the Red Sea, have added to concerns over potential supply disruptions and supported oil prices. European gas prices have declined by 5.5% despite supply outages in Norway adding to market volatility. Overall, volatility in the gas market seems to be stabilising at historical average levels, as Europe has managed to secure supplies from alternative sources and gas storage levels remain high. EU sanctions banning re-exports of Russian LNG through EU ports are expected to have a modest impact on the gas market as they do not affect EU imports directly and transhipped Russian volumes are relatively small. Metal prices have declined marginally, while food prices have declined by around 7%, driven by positive supply news for wheat crops and a continued moderation of cocoa prices.

In the United States, momentum in both activity and inflation has moderated. Real consumer spending was revised down for the first quarter of this year, and the latest monthly data suggest that consumption growth could be equally tepid in the second quarter. This represents a significant deceleration from the pace recorded in the second half of 2023. Moreover, 206,000 jobs were added in the non-farm sector in June, leading to a significant slowdown in the second quarter relative to the first quarter, confirming that the US labour market is cooling. Average hourly earnings growth has also fallen substantially from its peak in March 2022, but, at 3.9%, remains, as stated by Federal Reserve officials, incompatible with the 2% inflation target. Annual headline CPI inflation decreased to 3.0% in June, while core inflation fell marginally to 3.3%. Inflation momentum also weakened, notably in prices for non-rent services which had been a major driver of high inflation at the start of the year. At its June meeting, the Federal Open Market Committee maintained the target range for the federal funds rate at 5.25-5.5%. In its June economic projections, the Committee retained its outlook for a gradual deceleration in GDP growth but raised its headline and core inflation projections for 2024 and 2025 slightly, leaving its expectation of reaching its inflation target by the end of 2026 unchanged.

In China, economic growth is moderating as underlying weaknesses persist. Real GDP growth decelerated markedly to 0.7% quarter on quarter from 1.5% in the first quarter of 2024, as the real estate downturn has acted as a drag on consumer spending and the fiscal impulse from a late-2023 stimulus programme has faded. The release was somewhat below market consensus expectations. In year-on-year terms, GDP growth decreased to 4.7% from 5.3% in the first quarter. Moreover, monthly activity indicators for June showed a slump in retail sales and a further moderation in industrial production, both signalling a continued deceleration in the growth momentum at the end of the second quarter. Only exports have remained a growth driver, suggesting that the impact of proposed EU tariffs on Chinese exports will be limited. A new housing market support package marks a policy shift, although its impact on property-related activity cannot be observed yet. Looking ahead, the property market is expected to remain a drag on growth, with potential upside risk stemming from the new policy measures.

In the United Kingdom, growth picked up again while inflation fell to 2%. After stalling in April, economic activity increased by 0.4% month on month in May. Growth was particularly strong in services, although the industrial production and construction sectors also expanded. Overall, consumers’ resilience prevails in the face of persistently tight monetary conditions. UK headline CPI inflation declined to 2.0% in May. Energy prices are continuing to push inflation down, but as base effects unwind in the second half of the year, headline inflation is expected to increase again. Services inflation remained high and sticky. Contrary to expectations, momentum in services prices and wages has picked up again recently. In part, this likely reflects the increase in the national minimum wage in April, as well as the resilience in activity. The persistence in services inflation was one reason for the Bank of England to remain cautious at its June Monetary Policy Committee meeting and to hold its policy rate steady at 5.25%.

2 Economic activity

Real GDP rose by 0.3% quarter on quarter in the first quarter of 2024. This pick-up in growth, after five quarters of broadly stagnant activity, was led by services, while value added in industry contracted. The latest indicators, including from surveys, signal a continuation of the services-driven expansion in the second quarter. Given the weak industrial production data up to May, it is likely that the manufacturing sector continued to exert a drag on growth. Survey data suggest that production in industry remains fragile, as it is more exposed to the still tight monetary policy and global uncertainty. Overall, the euro area economy is expected to continue to recover over the course of this year mainly supported by consumption, driven by the strengthening of real incomes, resulting from lower inflation and higher nominal wages. Moreover, exports are anticipated to benefit from the improvement in global demand in the coming quarters, although external competitiveness challenges pose a potential downside risk. Finally, monetary policy should exert less of a drag on demand over time.

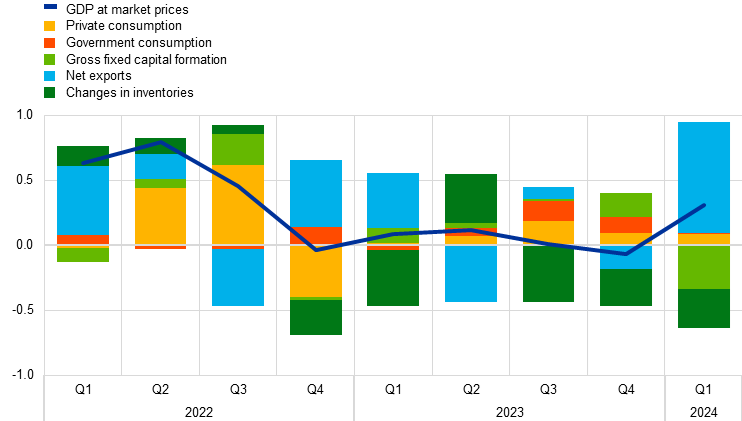

Real GDP grew by 0.3% quarter on quarter in the first quarter of 2024. Net trade contributed positively to growth, while domestic demand and changes in inventories made a negative contribution (Chart 3). Excluding the sharp fall in Irish non-construction investment, the contribution from domestic demand is estimated to have been slightly positive. The recovery in economic activity was driven by valued added in services.

Economic activity has continued to expand at a similar pace in the second quarter.[2] Incoming data suggest that real GDP growth likely continued to be services-driven in the second quarter. Industrial production contracted markedly in May, with levels in the first two months of the second quarter unchanged compared to the first quarter. The composite output Purchasing Managers’ Index (PMI) stood at 51.6 in the second quarter, up from 49.2 in the first quarter, thus indicating positive growth and continuing the upward movement started in late 2023. Across sectors, the PMI for manufacturing output remained in contractionary territory in the second quarter and data for June showed that the gains made in April and May have been wiped out. The PMIs for total new orders and new export orders were similarly weak and, given their more forward-looking content, this also points to weakness in the manufacturing sector in the third quarter (Chart 4, panel a). By contrast, the PMI for services output remained in expansionary territory in the second quarter, despite softening modestly in June (Chart 4, panel b). Moreover, services production was 0.7% above its first-quarter level in April.

Chart 3

Euro area real GDP and its components

(quarter-on-quarter percentage changes; percentage point contributions)

Sources: Eurostat and ECB calculations.

Note: The latest observations are for the first quarter of 2024.

Forward-looking survey data point to continued robust services in the third quarter of 2024. The European Commission’s business and consumer survey results for June suggest that expected demand for contact-intensive services for the next three months remains robust, particularly in travel services. The main findings from the ECB’s recent contacts with non-financial companies confirm this picture, with contacts reporting a strong tourist season and increasing signs of a modest consumption-led recovery (see Box 4Box 4). At the same time, there are mixed signals about whether the weakness in the manufacturing sector has bottomed out. Confidence in the industry sector remained stable overall in June as firms’ three-month-ahead production expectations and assessments of order books were largely unchanged. Nevertheless, the European Commission’s business survey indicates that more firms are reporting above-normal stocks of finished products, suggesting that demand for goods remains weak. At the same time, the ECB’s assessment of the main findings from its recent contacts with non-financial companies points to a bottoming out of aggregate manufacturing activity (see ). Looking ahead, trade tensions and geopolitical uncertainty will continue to pose headwinds for the manufacturing sector. However, positive factors supporting the recovery in economic activity persist. These include the continued strengthening of real incomes amid lower inflation and a favourable labour market, the increasing momentum of the services sector and the gradually fading drag of monetary policy on demand expected over time.

Chart 4

PMI indicators across sectors of the economy

a) Manufacturing | b) Services |

|---|---|

(diffusion indices) | (diffusion indices) |

|  |

Source: S&P Global Market Intelligence.

Note: The latest observations are for June 2024.

Employment continues to increase, supported by a growing labour force. Employment and total hours worked rose by 0.3% quarter on quarter in the first quarter of 2024 (Chart 5). Labour productivity remained unchanged as employment and hours worked increased at the same rate as GDP.[3] The implicit labour force, inferred from the unemployment rate and the number of unemployed, increased by 0.5% up to May this year and has been an important source of employment growth. The unemployment rate stood at 6.4% in May, unchanged from April, remaining at its lowest level since the euro was introduced. Labour demand remains at high levels, although the job vacancy rate fell slightly in the first quarter of 2024, to 2.8%, 0.1 percentage points lower than in the previous quarter.

Short-term labour market indicators point to ongoing employment growth in the second quarter of 2024. The monthly composite PMI employment indicator declined from 52.1 in May to 50.9 in June. The second-quarter average stands at 51.7, suggesting a further increase in employment (Chart 5). The positive perceptions of employment growth have been driven by the services sector, as construction and manufacturing remain in contractionary territory.

Chart 5

Euro area employment, the PMI assessment of employment and the unemployment rate

(left-hand scale: quarter-on-quarter percentage changes, diffusion index; right-hand scale: percentages of the labour force)

Sources: Eurostat, S&P Global Market Intelligence and ECB calculations.

Notes: The two lines indicate monthly developments, while the bars show quarterly data. The PMI is expressed in terms of the deviation from 50, then divided by 10. The latest observations are for the first quarter of 2024 for employment, June 2024 for the PMI assessment of employment and May 2024 for the unemployment rate.

Growth in private consumption remained modest at the start of 2024, but surveys suggest a strengthening of household spending dynamics. Private consumption grew by 0.2% in the first quarter, supported by a rebound in the consumption of goods, having shown very weak dynamics in 2023. Real disposable incomes increased in the first quarter of 2024, supported by the decline in inflation and robust nominal wage growth, amid a resilient labour market. The household saving ratio increased to 15.3% in the first quarter of 2024 (Chart 6, panel a), as the gains in income were made against a background of still elevated uncertainty and restrictive financing conditions, including tight standards for consumer credit. Incoming hard data for the second quarter show mixed signals about the momentum in goods consumption, with retail trade turnover increasing by 0.3%, but car registrations declining by 3.7% in April and May relative to their first-quarter levels. Surveys suggest that household spending growth will strengthen in the near term. The European Commission’s consumer uncertainty indicator declined and the consumer confidence indicator improved in June. However, the latter is still below its pre-pandemic average, reflecting subdued expectations for the economy and households’ own financial situations. Business expectations for demand in contact-intensive services over the next three months remain strong, while expected major purchases by consumers over the next 12 months have recovered to their pre-pandemic average (Chart 6, panel b). This evidence of an expected reduction in the divergence between consumer goods and services is supported by the results of the ECB’s latest Consumer Expectations Survey, which indicate that the propensity to spend on major items over the next 12 months is rising, while expected demand for tourist services remains high.

Chart 6

Private consumption, income and savings; expectations for retail trade, contact-intensive services and major purchases

a) Consumption, income and savings | b) Expectations |

|---|---|

(index: Q4 2019 = 100; percent) | (standardised percentage balances) |

|  |

Sources: Eurostat, European Commission and ECB calculations.

Notes: In panel a), income refers to household real adjusted disposable income and the household saving ratio is as a percentage of this income. In panel b), business expectations for demand in contact-intensive services and retail trade expectations refer to the next three months, while consumer expectations for major purchases refer to the next 12 months; the first series is standardised for the period January 2005-19, owing to data availability, whereas the other two series are for the period 1999-2019; “contact-intensive services” include accommodation, travel and food services. The latest observations are for the first quarter of 2024 for private consumption and June 2024 for expectations for contact-intensive services, retail trade and major purchases.

Business investment saw a moderate rise in the first quarter of 2024, and short-term indicators and surveys point to muted dynamics over the rest of 2024 (Chart 7, panel a). Non-construction investment (excluding Irish intangibles) rose by 0.5% quarter on quarter in the first quarter of 2024, recovering around 25% of its fall in the fourth quarter of 2023. Across assets, investment both in machinery and equipment and in intangibles had contributed positively to business investment since the pandemic. By contrast, according to the ECB’s recent contacts with non-financial companies, investment in transport equipment has been hampered by the continued uncertainty surrounding the green transition and the downsizing of energy-intensive industries (see Box 4). The PMIs for output and for new orders in the capital goods sector in the second quarter point to ongoing weakness in this category of business investment. The ECB’s recent bank lending survey and the ECB’s survey on the access to finance of enterprises in the euro area continued to report tight financing conditions in the second quarter. Feedback from the ECB’s corporate contacts suggests that firms continue to invest in cost-saving measures, in a context of labour shortages and strong global competition. However, they expect investment to remain subdued this year amid still elevated uncertainty. Similarly, the European Commission’s biannual investment survey suggests muted business investment growth in 2024 (see Box 3).

Chart 7

Real private investment dynamics and survey data

a) Business investment | b) Housing investment |

|---|---|

(quarter-on-quarter percentage changes; diffusion indices) | (quarter-on-quarter percentage changes; percentage balances and diffusion index) |

|  |

Sources: Eurostat, European Commission (EC), S&P Global Market Intelligence and ECB calculations.

Notes: Lines indicate monthly developments, while bars refer to quarterly data. The PMIs are expressed in terms of the deviation from 50. In panel a), business investment is measured by non-construction investment excluding Irish intangibles. The lines refer to responses from the capital goods sector. The latest observations are for the first quarter of 2024 for business investment and June 2024 for the PMIs. In panel b), the line for the European Commission’s activity trend indicator refers to the building and specialised construction sector’s assessment of the trend in activity over the preceding three months. The latest observations are for the first quarter of 2024 for housing investment and June 2024 for the European Commission survey and the PMIs.

Housing investment bounced back in the first quarter of 2024, but hard and soft indicators suggest that it likely contracted in the second quarter (Chart 7, panel b). Housing investment rose by 1.1% quarter on quarter in the first quarter, mostly owing to the favourable one-off effects of the mild weather in Germany and generous fiscal incentives in Italy. However, residential building permits stabilised at historically low levels, suggesting that pressures from projects in the pipeline were limited. Moreover, building and specialised construction output dropped by 0.4% in April 2024 compared with its average level in the first quarter of 2024. In addition, survey-based activity measures, such as the PMI for residential construction output and the European Commission’s indicator for building and specialised construction activity in the last three months, remained in contractionary territory up to June. The latter being mostly on account of a deterioration in demand. Overall, these developments suggest that housing investment is likely to have declined in the second quarter. Looking ahead, recent ECB surveys point to a moderation in the pace of decline. In the May Consumer Expectations Survey, household expectations for the housing market remained depressed, but more favourable than at the end of 2023, as reflected by the increased attractiveness of housing as a good investment. In the July Corporate Telephone Survey, construction companies reported ongoing depressed activity, but an expected recovery in the second half of 2024. In the July Bank Lending Survey, dynamics in credit standards and demand for housing loans are expected to improve.

Euro area exports stagnated in April 2024, despite the pick-up in foreign demand. Manufacturing export orders continued to contract sharply in June, while the services sector showed more resilience, with export orders remaining stable. The stagnation in export growth is in line with a broader trend of declining euro area market shares, exacerbated by the supply bottlenecks and energy price shocks – with the euro area being more affected given its high level of integration in global value chains and the domestic nature of the gas shock. Meanwhile, import growth has shown signs of recovery, with a 0.9% increase in import volumes of extra-euro area goods in April in three-month-on-three-month terms, amid stronger domestic consumption. Shipping costs are on the rise again, particularly between China and Europe, as global demand strengthens and firms frontload Christmas orders earlier than usual, owing to Red Sea disruptions and longer transportation times (see Box 4). Despite ongoing geopolitical tensions, there has been no discernible trend indicating a shift away from China as a primary sourcing country (see Box 1).

In summary, following the positive start to the year, activity in the euro area economy is expected to continue to recover over the course of 2024, despite lingering uncertainty. Trade tensions and geopolitical uncertainty will continue to pose headwinds for the manufacturing sector, and therefore for investment. However, declining inflation and robust wage growth are expected to underpin further increases in real disposable incomes, and thus in private consumption. In addition, euro area exports should pick up over the coming quarters in parallel with improvements in global growth. Finally, monetary policy should exert less of a drag on demand over time.

3 Prices and costs

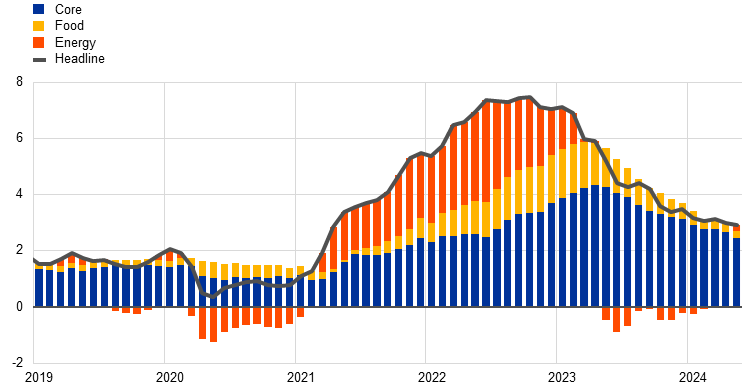

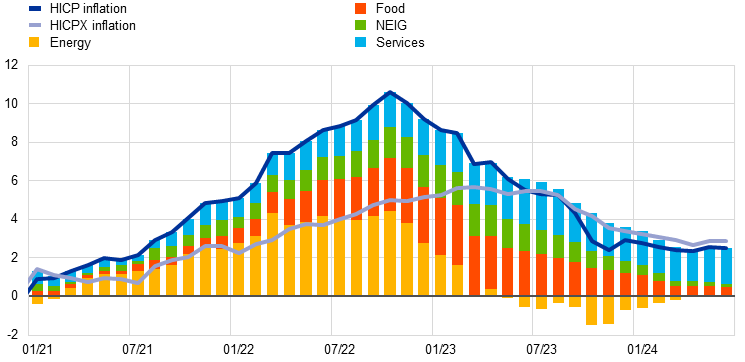

Euro area headline inflation stood at 2.5% in June 2024, down from 2.6% in May. Inflation excluding energy and food was 2.9% in June, unchanged from May but up from 2.7% in April. While some measures of underlying inflation ticked up in May owing to one-off factors, most measures were either stable or edged down in June. Domestic price pressures moderated in the first quarter of 2024, reflecting a stronger than expected decline in unit profits, while wage growth remained elevated. Measures of longer-term inflation expectations mostly stand at around 2%, while measures of shorter-term inflation expectations have decreased.

Euro area headline inflation, as measured in terms of the Harmonised Index of Consumer Prices (HICP), declined to 2.5% in June from 2.6% in May (Chart 8). The decrease was driven by lower inflation rates for food and energy. It followed an increase from 2.4% in April and confirmed earlier expectations that inflation would fluctuate around current levels, partly owing to energy-related base effects.

Chart 8

Headline inflation and its main components

(annual percentage changes; percentage point contributions)

Sources: Eurostat and ECB calculations.

Notes: NEIG refers to non-energy industrial goods. The latest observations are for June 2024.

Energy inflation decreased from 0.3% in May to 0.2% in June, having turned positive in May after almost a year of negative rates. The main drivers of the decrease were transport and liquid fuel prices. These reflect the recent decline of oil prices and a sharp decline in refining margins for petrol. Electricity and gas prices increased, but continued to contribute negatively to energy inflation.

Food inflation weakened further, falling to 2.4% in June from 2.6% in May. The decline was mainly driven by unprocessed food inflation (1.3% in June after 1.8% in May). Processed food inflation decreased slightly in June (to 2.7%, after 2.8% in May). The decline in the annual rate of change of food inflation was related to a downward base effect associated with the strong price increase in the more volatile unprocessed food component one year ago.

HICP inflation excluding energy and food (HICPX) stood at 2.9% in June, unchanged from May and up from 2.7% in April (Chart 9). In terms of components, non-energy industrial goods inflation stood at 0.7% in May and June, down from 0.9% in April. This is close to the pre-pandemic long-term average of 0.6%, suggesting a possible end to the gradual fading of the impact of past upward shocks. Services inflation was also unchanged between May and June, at 4.1%, having increased from 3.7% in April. The relatively greater persistence in services inflation compared with goods inflation is in line with strong wage growth and the more prominent role that labour costs play in the production of services. Meanwhile, indicators of underlying inflation showed mixed developments in May and June. Most exclusion-based measures edged up in May but some, such as HICP excluding unprocessed food and energy and HICPXX (which refers to HICPX inflation excluding travel-related items, clothing and footwear), decreased again in June. By contrast, domestic inflation ticked up marginally to 4.5% in June from 4.4% in May, remaining elevated at the top of the range of underlying inflation indicators. The Supercore indicator decreased slightly further, while the Persistent and Common Component of Inflation (PCCI) remained at the bottom of the range, at 1.7% in June, unchanged from May.

Chart 9

Indicators of underlying inflation

(annual percentage changes)

Source: Eurostat and ECB calculations.

Notes: The range of indicators of underlying inflation includes HICP excluding energy, HICP excluding unprocessed food and energy, HICPX, HICPXX, domestic inflation, 10% and 30% trimmed means, the PCCI, the Supercore indicator and a weighted median. The grey dashed line represents the ECB’s inflation target of 2% over the medium term. The latest observations are for June 2024.

Most indicators of pipeline pressures for goods inflation remained subdued but show signs of bottoming out (Chart 10). At the early stages of the pricing chain, producer price inflation for domestic sales of intermediate goods was still negative but less so than in the previous month (-2.9% in May after -3.9% in April). At the later stages of the pricing chain, the annual growth rates of producer prices for non-food consumer goods increased to 0.8% in May from 0.7% in April, while those in the consumer food segment increased to -0.4% from -0.9% over the same period. The gradual easing of pipeline pressures on industrial goods prices thus appears to have faded out. The annual growth rates of import prices for different goods categories have mostly remained negative but are moving upwards. The annual growth rate of import prices for energy increased substantially to 1.8% in May from ‑5.3% in April.

Chart 10

Indicators of pipeline pressures

(annual percentage changes)

Sources: Eurostat and ECB calculations.

Note: The latest observations are for April 2024 for import prices for non-food consumer goods and import prices for manufacturing of food products and for May 2024 for the rest.

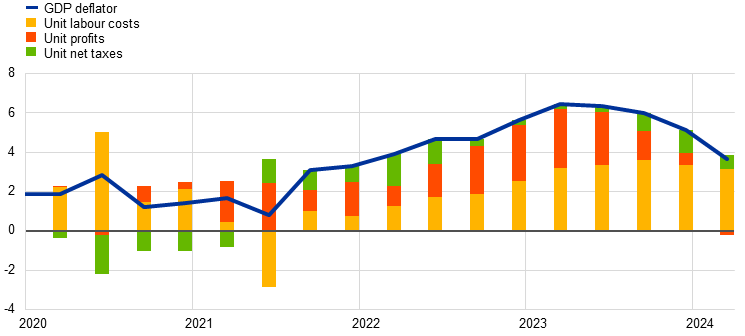

According to the data available at the time of the July Governing Council meeting, domestic cost pressures, as measured by growth in the GDP deflator, decreased to 3.6% in the first quarter of 2024 from 5.1% in the previous quarter, owing to smaller contributions from both labour costs and profits (Chart 11). After peaking at 6.5% in the first quarter of 2023, the annual growth rate of the GDP deflator eased further. The decline in the first quarter of 2024 was mainly driven by the decrease in unit profits growth, with the associated contribution dropping into negative territory, to -0.2 percentage points from 0.6 percentage points in the previous quarter. Similarly, the contribution of unit labour costs decreased further to 3.1 percentage points, from 3.3 percentage points in the previous quarter, masking a moderate increase in wage growth that was more than offset by rising productivity growth (-0.6% in the first quarter of 2024, up from -1.0% in the previous quarter). Overall, labour costs are still the main contributor to domestic price pressures.

Chart 11

Breakdown of the GDP deflator

(annual percentage changes; percentage point contributions)

Sources: Eurostat and ECB calculations.

Notes: The latest observations are for the first quarter of 2024. Compensation per employee contributes positively to changes in unit labour costs and labour productivity contributes negatively.

Wage pressures increased in the first quarter of 2024, and while they are expected to decline gradually, this will be from elevated levels. Data for the first quarter of 2024 show an increase in the annual growth rate of negotiated wages to 4.7%, up from 4.5% in the fourth quarter of 2023. Actual wage growth, according to the data available at the cut-off date and as measured by compensation per employee and compensation per hour, increased in the first quarter of 2024 to 5.0% and 5.4% respectively, up from 4.9% and 4.7% in the fourth quarter of 2023. The difference between actual and negotiated wage growth suggests that wage drift is playing a significant role.[4] The forward-looking wage tracker – which measures the wage growth of non-expired contracts – is broadly in line with expectations that negotiated wage growth in 2024 will, on average, be higher than in 2023 but will ease in 2025.[5]

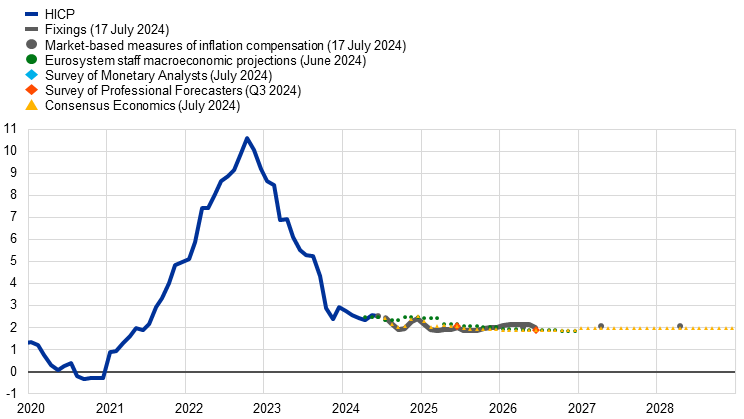

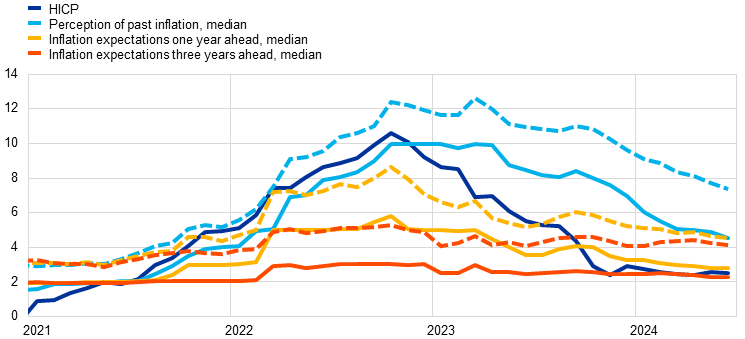

Survey-based indicators of longer-term inflation expectations and market-based measures of inflation compensation were broadly unchanged, with most standing at around 2.0% (Chart 12). In both the ECB Survey of Professional Forecasters (SPF) for the third quarter of 2024 and the June 2024 ECB Survey of Monetary Analysts (SMA), average and median longer-term inflation expectations (for 2028) remained unchanged at 2.0%. Market-based measures of inflation compensation (based on the HICP excluding tobacco) were broadly unchanged, with the five‑year forward inflation-linked swap rate five years ahead standing at around 2.3%. While these market‑based measures of inflation compensation include inflation risk premia and therefore do not directly gauge the genuine inflation expectations of market participants, model-based estimates of genuine inflation expectations, excluding inflation risk premia, indicate that market participants expect inflation to be around 2.0% in the longer term. Market-based measures of near-term euro area inflation outcomes suggest that investors expect inflation to stabilise at 2.0% from early 2025 onwards. The one-year forward inflation-linked swap rate one year ahead declined slightly over the review period to stand at 2.1%. On the consumer side, the June 2024 ECB Consumer Expectations Survey (CES) reported that the median rate of perceived inflation over the previous 12 months declined noticeably in June to 4.5%, from 4.9% in May. Meanwhile, median expectations for headline inflation over the next year remained unchanged, at 2.8%, from May to June, compared with 2.9% in April. Inflation expectations for three years ahead declined to 2.3% in May and June, from 2.4% in April. Inflation expectations at the one-year and three-year horizons remained below the perceived past inflation rate, suggesting that further disinflation is expected.

Chart 12

Headline inflation, inflation projections and expectations

a) Headline inflation, survey-based indicators of inflation expectations, inflation projections and market-based measures of inflation compensation

(annual percentage changes)

b) Headline inflation and ECB Consumer Expectations Survey

(annual percentage changes)

Sources: Eurostat, Refinitiv, Consensus Economics, CES, SPF, SMA, Eurosystem staff macroeconomic projections for the euro area, June 2024 and ECB calculations.

Notes: The market-based measures of inflation compensation series are based on the one-year spot inflation rate, the one-year forward rate one year ahead, the one-year forward rate two years ahead and the one-year forward rate three years ahead. The observations for market-based measures of inflation compensation are for 17 July 2024. Inflation fixings are swap contracts linked to specific monthly releases in euro area year-on-year HICP inflation excluding tobacco. The SPF for the third quarter of 2024 was conducted between 2 and 5 July 2024. The cut-off date for the Consensus Economics long-term forecasts was July 2024. For the CES, dashed lines represent the mean and solid lines the median. The cut-off date for data included in the Eurosystem staff macroeconomic projections was 15 May 2024. The latest observations are for June 2024.

4 Financial market developments

Over the review period from 6 June to 17 July 2024, developments in euro area financial markets reflected expectations for the path of inflation and the potential for further monetary policy rate cuts in the coming months. In the weeks following the Governing Council’s decision to lower the key ECB policy rates by 25 basis points at its June meeting, the euro area risk-free curve shifted down, with investors pricing in a further 46 basis points of cumulative cuts by the end of 2024. The option-implied volatility of policy rate expectations remained at elevated levels, although well below the peaks seen in late 2022 and early 2023. Euro area sovereign bond market movements were driven by national elections. Despite initial volatility, changes in sovereign spreads had largely unwound by the end of the review period. Euro area equity prices decreased for both financial and non-financial corporations, on the back of somewhat less favourable risk sentiment in the euro area. Euro area corporate bond spreads widened for high-yield corporations and were broadly stable for investment-grade firms. In foreign exchange markets, the euro appreciated slightly against the US dollar and in trade-weighted terms.

Euro area near-term risk-free rates have declined marginally since the June Governing Council meeting. The euro short-term rate (€STR) averaged 3.7% over the review period, following the Governing Council’s widely anticipated decision to lower the key ECB interest rates by 25 basis points at its June meeting. Excess liquidity decreased by around €131 billion between 6 June and 17 July to stand at €3,071 billion. This mainly reflected repayments in June of the third series of targeted longer-term refinancing operations (TLTRO III) and, to a lesser degree, the decline in the asset purchase programme (APP) portfolio, as the Eurosystem no longer reinvests the principal payments from maturing securities under this portfolio. The overnight index swap (OIS) forward curve, which is based on the €STR, declined by around 20 basis points for maturities of one year and 26 basis points for maturities of two years, reflecting, overall, expectations of a more marked easing of monetary policy. Despite the overall decline, financial markets were pricing in tighter monetary policy in the early part of the review period. These movements were reversed following softer data releases, in particular, a lower-than-expected June inflation reading in the United States, and deteriorating risk sentiment in Europe associated with political uncertainty in France. The option-implied volatility of short-term forward rates increased slightly but remained well below the peaks recorded in late 2022 and early 2023. At the end of the review period, markets had priced in cumulative rate cuts of around 46 basis points by the end of 2024. Longer-term euro area risk-free rates decreased during the review period. For example, the ten-year nominal euro area risk-free rate stood at 2.5%, ending the review period with an overall decrease of 12 basis points.

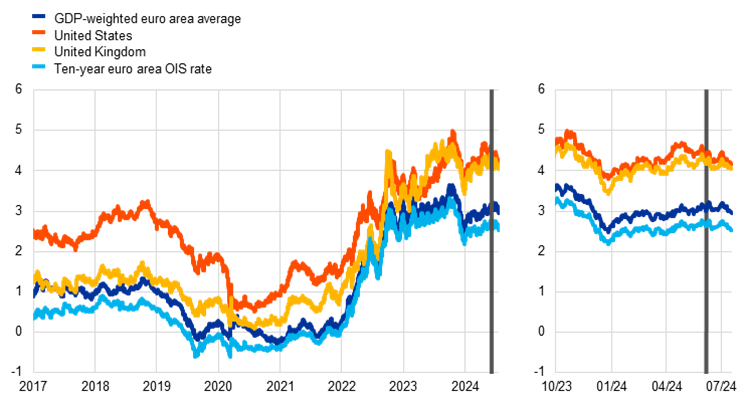

Long-term sovereign bond yield spreads to risk-free rates widened very slightly amid political uncertainty in France (Chart 13). The ten-year GDP-weighted euro area sovereign bond yield closed the review period at 3.0%, 10 basis points lower than at the beginning of the review period, implying that the spread over the ten-year euro area risk-free rate had remained almost unchanged, having widened by only 2 basis points. This widening of the GDP-weighted spread was largely driven by movements in the French sovereign spread to the OIS, which widened by 15 basis points in the review period following the announcement on 9 June of snap parliamentary elections. The rise in French sovereign spreads, which increased by as much as 22 basis points, initially spilled over to other euro area sovereigns, while the German sovereign spread declined on account of flight-to-quality flows. By the end of the review period, movements in other euro area sovereigns had broadly unwound, with the Italian sovereign spread standing 3 basis points lower, the German sovereign spread unchanged, and other sovereigns seeing similarly negligible movements. Abroad, the ten-year US Treasury yield declined by 13 basis points to 4.2%, while the ten-year UK sovereign bond yield decreased by 10 basis points to 4.1%.

Chart 13

Ten-year sovereign bond yields and the ten-year OIS rate based on the €STR

(percentages per annum)

Sources: LSEG and ECB calculations.

Notes: The vertical grey line denotes the start of the review period on 6 June 2024. The latest observations are for 17 July 2024.

Euro area corporate bond spreads widened for high-yield corporations and were broadly stable for investment-grade firms. By the end of the review period, spreads for investment-grade firms had widened by only 1 basis point. By contrast, spreads of euro area firms in the high-yield segment had widened by 23 basis points amid higher risk aversion, driven by both financial and non-financial corporations.

Euro area equity prices declined for both financial and non-financial corporations, owing to worsening risk sentiment in the euro area. Over the review period, broad stock market indices in the euro area declined by 3.4%, in contrast with their US counterparts, which increased by 4.5%. In net terms, the equity prices of euro area non-financial corporations declined by 4.4%, while the equity prices of euro area banks and other financial corporations declined by 0.8% and 1.2% respectively, with French corporations being particularly affected. In the United States, equity prices increased across the board, up by 4.0% for non-financial corporations, 11.1% for banks and 7.5% for other financial corporations.

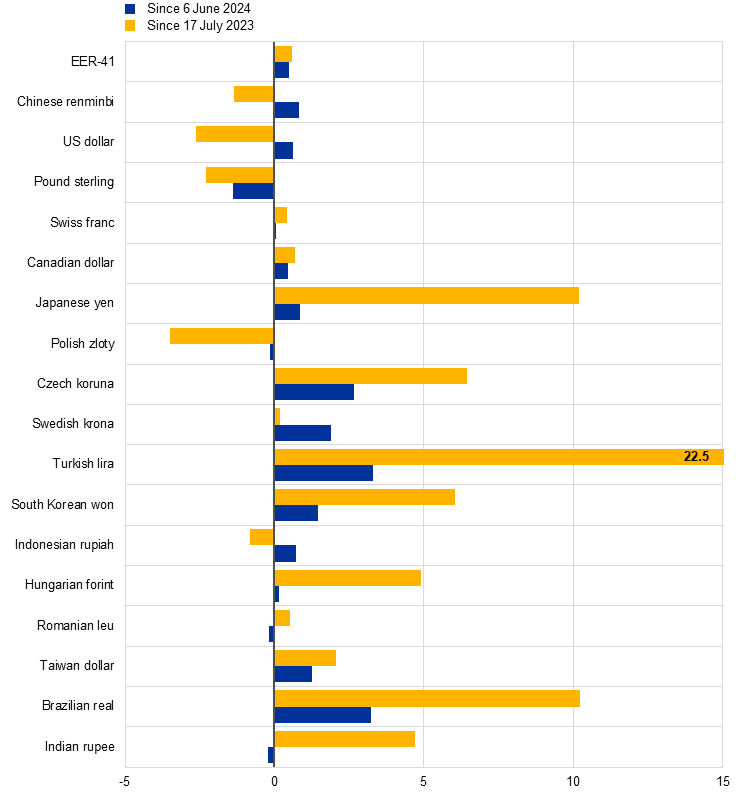

The euro exchange rate appreciated slightly against the US dollar (+0.6%) and in trade-weighted terms (+0.5%) (Chart 14). At the beginning of the review period, the US dollar strengthened in nominal terms, up to the levels of October 2023. This was supported by a still resilient labour market and the outcome of the Federal Open Market Committee meeting in June, which was perceived as (slightly) hawkish. At the same time, softer-than-expected consumer price index reports for May and June tempered the US dollar’s performance, which depreciated by 0.6% overall by the end of the review period. During the review period, the nominal effective exchange rate of the euro – as measured against the currencies of 41 of the euro area’s most important trading partners – appreciated slightly (+0.5%). The euro depreciated against the pound sterling (-1.4%), as expectations of a summer interest rate cut by the Bank of England weakened. In contrast, the euro appreciated against the Chinese renminbi (+0.8%), and further appreciated against the Swedish krona (+1.9%) and the Canadian dollar (+0.5%), with the latter appreciation supported by the Bank of Canada’s rate cut in June. Finally, the euro appreciated against the Japanese yen (+0.9%). The Japanese yen stood at a 30-year low against the US dollar during the review period but appreciated sharply on 11 and 12 July, following what market participants suspected to be foreign exchange interventions.

Chart 14

Changes in the exchange rate of the euro vis-à-vis selected currencies

(percentage changes)

Source: ECB calculations.

Notes: EER-41 is the nominal effective exchange rate of the euro against the currencies of 41 of the euro area’s most important trading partners. A positive (negative) change corresponds to an appreciation (depreciation) of the euro. All changes have been calculated using the foreign exchange rates prevailing on 17 July 2024.

5 Financing conditions and credit developments

In May 2024 composite euro area bank funding costs and bank lending rates remained at high levels. Growth rates for bank loans to firms and to households remained stable at levels close to zero, reflecting high lending rates, weak economic growth and tight credit standards. Over the period from 6 June to 17 July 2024, the cost to non-financial corporations (NFCs) of market-based debt declined, while the cost of equity financing increased. According to the July 2024 euro area bank lending survey, credit standards tightened slightly in the second quarter of this year, while standards for mortgages eased moderately. Firms’ demand for loans fell slightly, while households’ demand for mortgages rose for the first time since early 2022. According to the latest Survey on Access to Finance of Enterprises (SAFE), fewer euro area firms indicated a tightening of financing conditions in the second quarter compared with the first quarter. The annual growth rate of broad money (M3) continued its gradual recovery, supported by net foreign inflows.

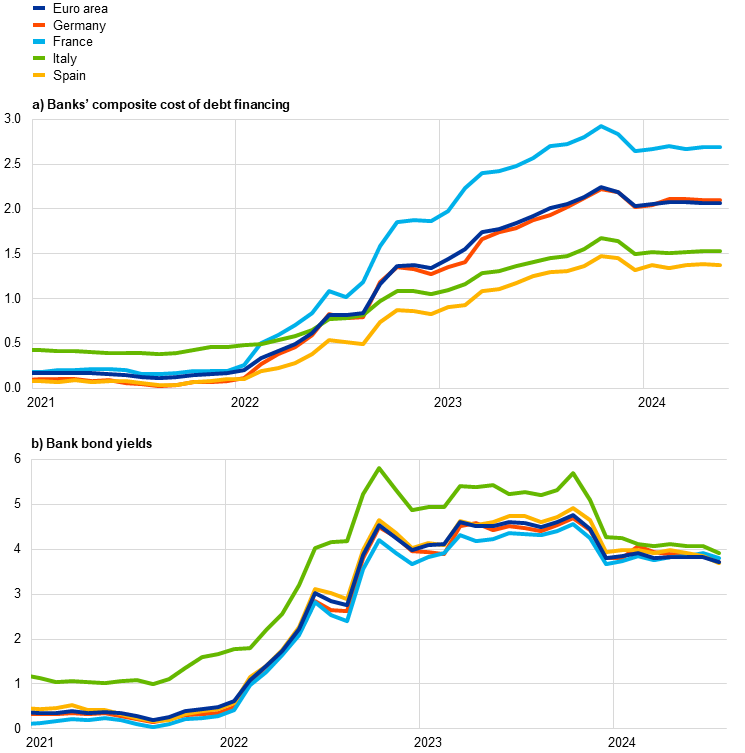

Euro area bank funding costs remained high by historical standards. The composite funding cost of debt financing for euro area banks remained unchanged in May, standing at 2.07% (Chart 15, panel a). Bank bond yields remained broadly stable between May and July (Chart 15, panel b), despite an uptick of bank bond spreads owing to the increase in political uncertainty as to the outcome of the European and French elections. Aggregate deposit rates, which account for the largest share of bank funding costs, remained steady overall in May, although this masks considerable cross-country heterogeneity. Time deposit rates decreased marginally, while overnight deposit rates remained broadly unchanged, resulting in a slight narrowing of the large spread between the two. Rates on deposits redeemable at a period of notice of up to three months remained constant, while those with notice of more than three months increased marginally.

Central bank lending operations continued to decline smoothly, contributing to higher bank funding costs. Banks have made further repayments (both mandatory and voluntary) of funds borrowed under the targeted longer-term refinancing operations (TLTROs). On 26 June repayments of €64.5 billion were made on the third series of operations (TLTRO III). A total of €2.037 trillion TLTRO III funds have been repaid since the recalibration of the terms and conditions came into effect on 23 November 2022, amounting to a 96% reduction in outstanding amounts.[6] Amid the winding-down of TLTROs and the decline in deposits, banks have increased their issuance of bonds, these being remunerated above deposit and policy rates.

Bank balance sheets have been robust overall, despite a weak economic environment and increased uncertainty. In the first quarter of 2024 banks continued to improve their capitalisation and maintained capital ratios well above Common Equity Tier 1 (CET1) requirements, ensuring a well-capitalised banking system capable of meeting the sustainable credit needs of the real economy. Bank profitability remained high in the first quarter, against a backdrop of still relatively low loan loss provisions and wide interest rate margins. However, loan-deposit margins on new business and outstanding amounts progressively declined up to May, falling from the peaks observed in mid-2023. Non-performing loans (NPLs) continued to gradually increase from the low levels seen in the first quarter of this year. The number of corporate insolvencies and the share of underperforming (i.e. Stage 2) loans, especially for small firms, has slightly risen, pointing to further increases in NPLs, worsening asset quality and higher provisioning costs for banks looking ahead.

Chart 15

Composite bank funding costs in selected euro area countries

(annual percentages)

Sources: ECB, S&P Dow Jones Indices LLC and/or its affiliates, and ECB calculations.

Notes: Composite bank funding costs are a weighted average of the composite cost of deposits and unsecured market-based debt financing. The composite cost of deposits is calculated as an average of new business rates on overnight deposits, deposits with an agreed maturity and deposits redeemable at notice, weighted by their respective outstanding amounts. Bank bond yields are monthly averages for senior tranche bonds. The latest observations are for May 2024 for the composite cost of debt financing for banks and for 17 July 2024 for bank bond yields.

Bank lending rates for firms and households remained at high levels. In May lending rates for firms decreased to 5.10%, down from 5.18% in the previous month and below the peak of 5.27% reached in October 2023 (Chart 16), amid heterogeneity across euro area countries and maturities. The decline in lending rates for firms in May was more pronounced for loans with short interest rate fixation periods (up to one year), while rates with longer fixation periods of over one year saw a slight increase. The spread between interest rates on small and large loans to euro area firms is still narrow but increased by 0.43 percentage points in May, as compared with April when it hit its lowest level since the pandemic, and reflects lower rates on large loans and higher rates on small loans. Lending rates on new loans to households for house purchase saw no change for the third month in a row, standing at 3.80% in May, which is still a high level historically but below the peak of 4.02% seen in November 2023 (Chart 16). Interest rates on new loans to households for consumption edged up in May, showing signs of stabilisation at high levels amid some volatility, while rates for loans to sole proprietors remained stable.

Chart 16

Composite bank lending rates for NFCs and households in selected countries

(annual percentages)

Sources: ECB and ECB calculations.

Notes: Composite bank lending rates are calculated by aggregating short and long-term rates using a 24-month moving average of new business volumes. The latest observations are for May 2024.

Over the period from 6 June to 17 July 2024, the cost to NFCs of market-based debt declined, while their cost of equity financing increased. Based on the available monthly data, the overall cost of financing for NFCs – i.e. the composite cost of bank borrowing, market-based debt and equity – remained at 6.2% in May, virtually unchanged from its level in April and lower than the multi-year high reached in October 2023 (Chart 17).[7] None of the cost components showed any significant change, other than the cost of bank loans, which saw a decline for short-term loans and a marginal increase for loans with a maturity of more than one year. Daily data from 6 June to 17 July 2024 confirm a fall in the cost of market-based debt, owing to a decline in the risk-free interest rate – as approximated by the ten-year overnight index swap rate – that was not offset by the marginal widening of spreads on bonds issued by NFCs, especially in the high yield segments. Notwithstanding the decline in the risk-free rate, the cost of equity financing increased over the same period, reflecting a significant increase in the equity risk premium.

Chart 17

Nominal cost of external financing for euro area NFCs, broken down by component

Sources: ECB, Eurostat, Dealogic, Merrill Lynch, Bloomberg, Thomson Reuters and ECB calculations.

Notes: The overall cost of financing for non-financial corporations (NFCs) is based on monthly data and is calculated as a weighted average of the cost of borrowing from banks (monthly average data), market-based debt and equity (end-of-month data), based on their respective outstanding amounts. The latest observations are for 17 July 2024 for the cost of market-based debt and the cost of equity (daily data), and for May 2024 for the overall cost of financing and the long and short-term cost of bank borrowing (monthly data).

In May 2024 the annual growth rates of bank lending to firms and to households remained stable at levels close to zero, reflecting high lending rates, weak economic growth and tight credit standards. Annual growth in loans to NFCs and to households stood at 0.3% in May, marginally up from the 0.2% seen in April for both sectors (Chart 18). These annual growth rates have fluctuated around these low levels since the beginning of 2024. The ongoing weakness in loan growth follows the subdued lending dynamics observed since the beginning of 2023, on the back of weak aggregate demand, tight credit standards and the dampening impact of monetary policy restriction as a result of higher lending rates. Mortgage loan growth remained muted, while consumer credit has been relatively resilient and other lending to households, which includes loans to sole proprietors, continued to contract, albeit at a slowing pace. The ECB’s Consumer Expectations Survey in May 2024 showed that a still large but declining net percentage of survey respondents reported that credit access had become harder over the previous 12 months and expected it to become even more difficult over the next 12 months.

Chart 18

MFI loans in selected euro area countries

(annual percentage changes)

Sources: ECB and ECB calculations.

Notes: Loans from monetary financial institutions (MFIs) are adjusted for loan sales and securitisation; in the case of non-financial corporations (NFCs), loans are also adjusted for notional cash pooling. The latest observations are for May 2024.

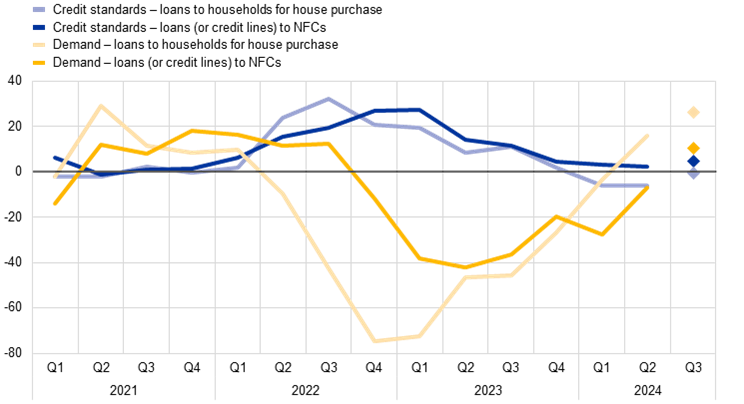

According to the July 2024 euro area bank lending survey, banks reported a small further tightening of their credit standards for loans to firms and a moderate further easing for loans to households for house purchase in the second quarter of 2024 (Chart 19). The tightening of credit standards for firms, which was accompanied by a further increase in the share of rejected loan applications, adds to the substantial cumulative tightening seen since 2022. Bank risk tolerance was the main driver behind the net tightening, while bank risk perceptions were less relevant than during the rate hiking cycle. Net tightening in credit standards was reported in France and in Germany, while only Italian banks reported a net easing. Banks also reported an increase in rejection rates and a further tightening of credit standards for consumer credit, driven primarily by risk perceptions linked to the economic outlook and borrower credit worthiness. The easing reported for housing loans was driven by competitive pressures and coincided with a decrease in the share of rejected applications. Euro area banks expect a further moderate tightening for loans to firms and broadly unchanged credit standards for loans to households in the third quarter of 2024.

Chart 19

Changes in credit standards and net demand for loans to NFCs and loans to households for house purchase

(net percentages of banks reporting a tightening of credit standards or an increase in loan demand)

Source: Euro area bank lending survey.

Notes: For survey questions on credit standards, “net percentages” are defined as the difference between the sum of the percentages of banks responding “tightened considerably” and “tightened somewhat” and the sum of the percentages of banks responding “eased somewhat” and “eased considerably”. For survey questions on demand for loans, “net percentages” are defined as the difference between the sum of the percentages of banks responding “increased considerably” and “increased somewhat” and the sum of the percentages of banks responding “decreased somewhat” and “decreased considerably”. The diamonds denote expectations reported by banks in the current round. The latest observations are for the second quarter of 2024.

Banks reported a further decline in demand for loans by firms and an increase in demand for loans by households in the second quarter of 2024. The decline in firm loan demand, which was substantially smaller than in the previous quarter, was mainly driven by high interest rates and weak fixed investment, while there was also a small positive contribution from inventories and working capital. The demand for both housing loans and consumer credit increased for the first time since mid-2022, driven mainly by improved housing market prospects, consumer confidence and spending on durables. The increase in net demand for housing loans was weaker than banks had expected in the previous quarter, but stronger for consumer credit. For the third quarter of 2024, banks expect moderate growth in demand for loans to firms which, if it were to materialise, would be the first seen since the third quarter of 2022. Moreover, they expect a rise in demand for loans to households, that demand being substantially higher for housing loans than for consumer credit.

According to the banks surveyed, access to funding improved in most market segments but is expected to deteriorate across all segments over the third quarter of 2024. Bank access to funding improved for debt securities and – to a lesser extent – for money markets. Access to retail funding remained broadly unchanged overall but continued to deteriorate slightly for short-term funding. The deterioration in access to funding anticipated for the third quarter of 2024 was driven by French banks, potentially reflecting increased political uncertainty given that the survey was conducted after the French snap parliamentary elections were announced but before the first round of those elections took place.

Perceived credit risks in bank loan portfolios had a moderate tightening impact on bank lending conditions in the first half of 2024, while credit standards for firms displayed some heterogeneity across economic sectors, tightening strongly in commercial real estate. Banks reported that NPL ratios and other indicators of credit quality had a net tightening effect on credit standards for loans to firms and for consumer credit in the first half of 2024, and had a broadly neutral impact on housing loans. As in the past, the main factors behind the contribution of NPL ratios to tightening lending conditions were the higher risk perceptions and lower risk tolerance of banks, as well as the greater pressure exerted by supervisory or regulatory requirements. Credit standards for firms tightened further in all economic sectors in the first half of 2024, ranging from a very small net tightening in services and manufacturing to a relatively large net tightening in commercial real estate. Banks also reported a net decrease in demand for loans and credit lines in most economic sectors, except in services. In the second half of 2024 euro area banks expect a net tightening in lending conditions, combined with a moderate net increase in loan demand in most economic sectors, except in construction and commercial real estate.

Climate risks and related policy measures continued to contribute to a tightening of lending conditions for brown firms. Euro area banks indicated that firms’ climate-related risks and measures to cope with climate change continued to have a net tightening impact on lending policies for loans to brown firms (i.e. firms that contribute significantly to climate change and have not yet started, or have made little progress, with transition) over the past 12 months, although by less than expected. By contrast, the same factors had a further net easing impact for loans to green firms (i.e. firms that do not contribute or contribute little to climate change) and firms in transition (i.e. firms that contribute to climate change but are making considerable progress with transition). Physical risk was reported by banks as being the main driver of the tightening impact on their lending policy. Over the next twelve months, euro area banks expect a slightly stronger net tightening impact on credit standards for loans to brown firms, while a slightly stronger net easing impact is expected for green firms and firms in transition.

According to the SAFE, fewer euro area firms indicated a tightening of financing conditions in the second quarter of 2024 compared with the first quarter. The net percentages of firms reporting increases in interest rates on bank loans and in other financing costs, such as charges, fees and commissions, both declined, falling respectively to 31% (down from 43% in the previous quarter) and to 28% (after 37% previously). As in the first quarter of 2024, few firms reported obstacles to obtaining a bank loan.

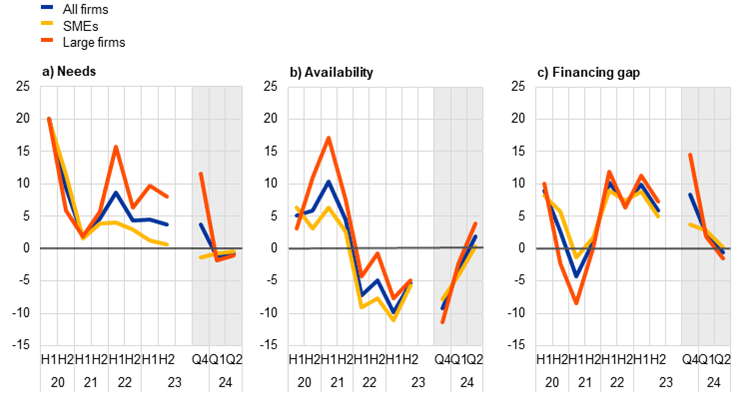

Firms also signalled a small improvement in the availability and a slight reduction in the need for bank loans, resulting in a small decrease in their bank financing gap. The net percentage of firms reporting an improvement in the availability of bank loans was 2% in the second quarter of 2024, in contrast with a net 3% of firms that reported a deterioration in the previous quarter (Chart 20). This change is mainly attributable to large firms given that, on average, small and medium-sized enterprises (SMEs) reported no changes. In the second quarter a net 1% of firms reported lower bank loan needs (stable from the previous quarter) across all firm sizes. Consequently, the change in the financing gap – the estimated difference between the change in the need for bank loans and the change in bank loan availability – was negative for a net 1% of firms, down from 2% of firms for which it was positive in the previous quarter. However, across firm sizes, the change in the financing gap was negative for a net 2% of large firms, while remaining stable for SMEs. Looking ahead, firms expect a further improvement in the availability of external financing over the next three months, with larger firms being more optimistic than SMEs.

Chart 20

Changes in euro area firms' bank loan needs and availability and financing gap

(net percentages of respondents)

Sources: SAFE and ECB calculations.

Notes: SMEs stands for small and medium-sized enterprises. The figures are based on firms for which the instrument in question is relevant (i.e. they have used it or considered using it). Respondents replying “not applicable” or “don’t know” are excluded. Net percentages are the difference between the percentage of firms reporting an increase for a given factor and the percentage reporting a decrease. The figures refer to rounds 23 to 31 of the SAFE (April-September 2020 to April-June 2024). On the x-axis, H1 stands for the reference period running from quarter 2 to quarter 3 and H2 for the reference period running from quarter 4 to quarter 1 of the next year. The grey shaded charts reflect responses to the same question but on a quarterly basis. The financing gap indicator combines both financing needs and the availability of bank loans at firm level. The indicator of the perceived change in the financing gap takes a value of 1 (-1) if the need increases (decreases) and availability decreases (increases). If firms perceive only a one-sided increase (decrease) in the financing gap, the variable is assigned a value of 0.5 (-0.5). A positive value for the indicator points to a widening of the financing gap. Values are multiplied by 100 to obtain weighted net balances in percentages.

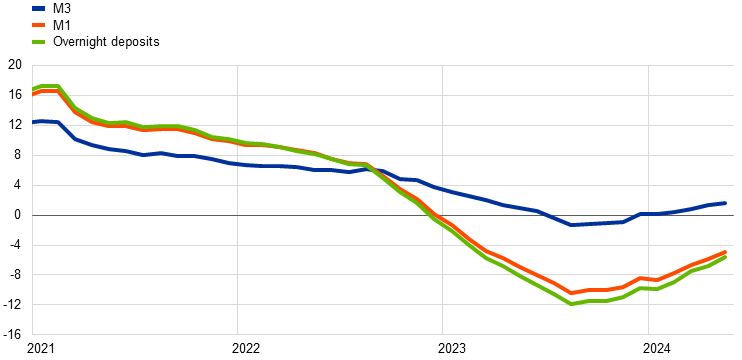

Firms and households recorded a further increase in time deposit volumes in May 2024, although the reallocation from overnight deposits has been gradually slowing. Overnight deposit volumes contracted at a slowing pace in May, the annual growth rate rising to ‑5.6%, up from ‑6.8% in April (Chart 21). The ongoing preference among firms and households for holding time deposits and marketable instruments continues to be explained by the still substantially higher remuneration of these instruments compared with overnight deposits. While deposit flows are still significantly more tilted towards time deposits than in the past, this reallocation is losing steam, with the spread between the returns on both instruments stabilising. Firms’ deposit allocation is moving closer to a level that is more consistent with historical patterns, and three consecutive positive, albeit contained, monthly inflows into overnight deposits were recorded between March and May. At the same time, deposit inflows from firms and households were partly offset by outflows from money market funds, amid the decline in short-term interest rates seen in May.

Chart 21

(annual percentage changes, adjusted for seasonal and calendar effects)

Source: ECB.

Note: The latest observations are for May 2024.

The annual growth rate of broad money (M3) in the euro area continued its gradual recovery in May 2024, supported by net foreign inflows. Money growth has been gradually increasing since the beginning of 2024. In May M3 growth increased to 1.6%, up from 1.3% in April (Chart 21). Annual growth of narrow money (M1) – which comprises the most liquid assets of M3 – stayed in negative territory but continued to increase to ‑4.9% in May, compared with ‑5.9% in April. Foreign inflows remained the only consistent positive driver of money growth, amid stagnant lending to households and firms, the continuing contraction of the Eurosystem balance sheet and the issuance of bank bonds in a context of ongoing repayments of TLTRO funds.

Boxes

1 Geopolitics and trade in the euro area and the United States: a de-risking of import supplies?

In recent years, a series of adverse shocks has highlighted vulnerabilities related to the sourcing of imported goods. In response, some firms in both the euro area and the United States have changed (or are planning to change) their sourcing strategies to improve supply-chain resilience.[8] Based on detailed product-level data, this box analyses the extent to which and how the euro area and the United States have modified their sourcing strategies since 2016 – when geopolitical considerations began to play a stronger role in trade relations and de-risking concerns arose[9] – and the potential impact on import prices. It focuses on two different, but not mutually exclusive, sourcing strategies aimed at fostering supply-chain resilience and addressing national security concerns: diversification (increasing the number of supplier countries) and rebalancing (reducing the market share of the main supplier country).[10]

More2 Recent country-specific and sectoral developments in labour productivity in the euro area

A combination of various adverse shocks has contributed to productivity growth being suppressed in the euro area over the last four years. The pandemic, along with disruptions in global supply chains and the energy price increases from 2021, which were aggravated by the Russian war in Ukraine, have all contributed to the slowdown in productivity growth. These factors have exerted a particularly significant impact on the industry, wholesale and retail trade, and construction sectors. As a result, productivity dynamics have been weaker than in the past, with average productivity per person employed declining by 0.2% on average per year since the fourth quarter of 2019 compared with average growth of 0.8% per year before the pandemic. The average growth rate of productivity per hour since the fourth quarter of 2019 amounted to 0.2% per year, compared with average growth of 1.2% per year before the pandemic. In the first quarter of 2024 productivity per person employed was 0.7% lower than in the fourth quarter of 2019 and productivity per hour worked was higher by just 0.7% (Chart A).

More3 What do recent surveys reveal about euro area business investment in 2024?

This box assesses the outlook for euro area business investment in 2024 according to recent surveys conducted by the European Commission and the European Investment Bank. Euro area business investment decelerated considerably in 2023 in the wake of the pandemic, the 2022-23 energy crisis and the subsequent tightening of financing conditions in succession. After contracting sharply in the final quarter of 2023, investment ticked up modestly in the first quarter of 2024. The June 2024 Eurosystem staff macroeconomic projections for the euro area point to subdued annual investment growth in 2024, which is broadly in line with the results of the surveys.

More4 Main findings from the ECB’s recent contacts with non- financial companies

This box summarises the findings of recent contacts between ECB staff and representatives of 62 leading non-financial companies operating in the euro area. The exchanges took place between 17 and 26 June 2024.[11]

Contacts reported a gradual pick-up in activity in the second quarter of the year, amid increasing signs of a modest, consumption-led recovery (Chart A and Chart B, panel a). Growth was still led by services, but manufacturing activity was bottoming out and construction was showing first signs of stabilisation. The investment outlook remained subdued, however, with uncertainty remaining high. Growth in the euro area still lagged that in the United States and Asia, but contacts also pointed to weaker than expected growth in China and its consequences for global prices and competition. Within the euro area, growth in southern Europe continued to outpace that in northern Europe.

More5 The dynamics of inflation differentials in the euro area

The surge in euro area inflation in 2021 and 2022 came with a sizeable increase in inflation dispersion across countries. Persistent inflation divergences across euro area countries can have implications for the transmission of the single monetary policy. The ECB therefore monitors developments in, as well as the nature of, inflation differentials. This box explores this issue with a focus on the recent inflation surge.

More6 Selling price expectations for services: what do they tell us about consumer price pressures?