Derivatives-related liquidity risk facing investment funds

Published as part of Financial Stability Review, May 2020.

Stricter margining requirements for derivative positions have increased the demand for collateral by market participants in recent years. At the same time, euro area investment funds which use derivatives extensively have been reducing their liquid asset holdings. Using transaction-by-transaction derivatives data, this special feature assesses whether the current levels of funds’ holdings of cash and other highly liquid assets would be adequate to meet funds’ liquidity needs to cover variation margin calls on derivatives during stressed market periods, once the derivative portfolios become fully collateralised. The evidence so far indicates that euro area funds were able to meet the fivefold increase in variation margin during the height of the coronavirus-related market stress. But some of them were likely to have done so by engaging in repo transactions, selling assets and drawing on credit lines, thus amplifying the recent market dynamics.

1 Introduction

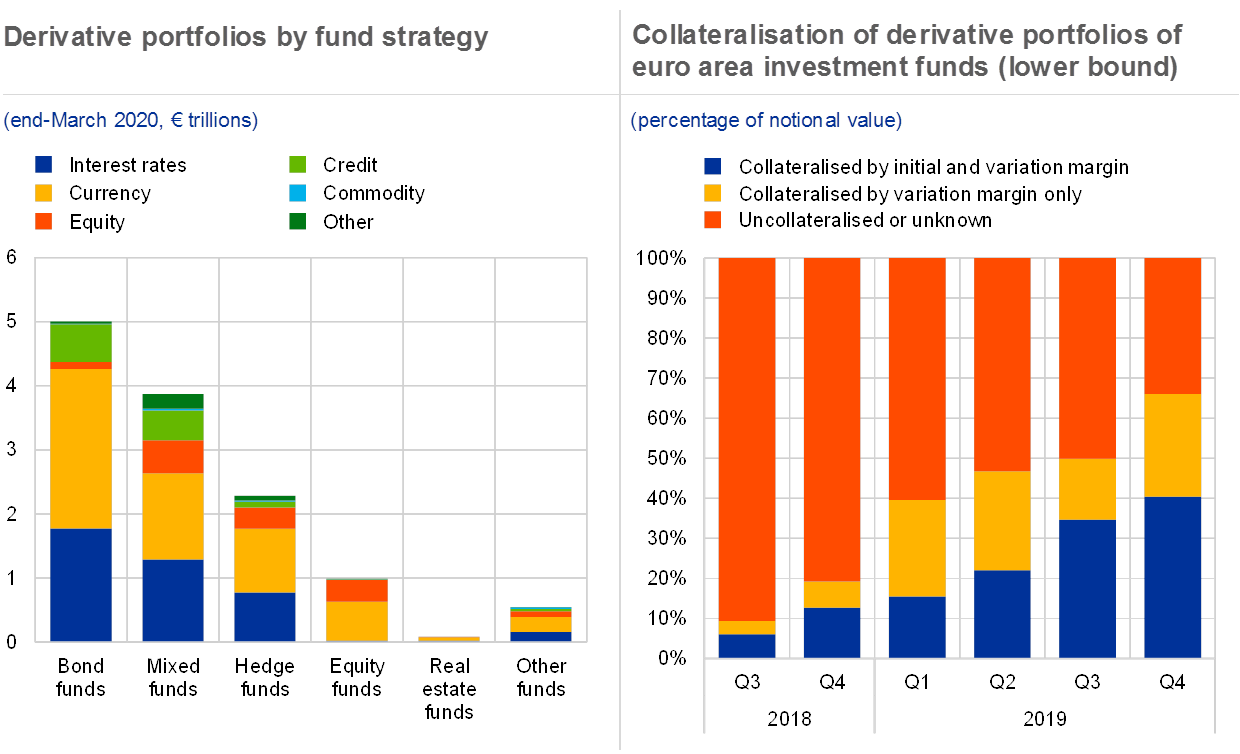

Out of the almost 60,000 euro area investment funds, around 35% use derivatives. For instance, two-thirds of funds with a net asset value above €500 million have a derivative exposure. At the end of March 2020, the notional value of euro area funds’ derivative exposures stood at almost €13 trillion and was concentrated in a few euro area countries, namely Luxembourg (53%), Germany (20%) and Ireland (18%), all of which also have a sizeable fund sector. Interest rate, equity and foreign exchange (FX) derivatives together accounted for almost 90% of the notional value. Funds use derivatives either for hedging purposes or to increase their potential exposure to risky assets, and the composition of their derivative portfolios depends heavily on their mandates (see Chart B.1, left panel).

Recent regulatory reform in the derivatives market has introduced the daily exchange of margin for the vast majority of derivative exposures. The exchange of margin in the form of high-quality collateral reduces counterparty credit risk. But the requirements also increase liquidity risk as counterparties need to meet margin calls with high-quality collateral at short notice. In the prevailing low-yield environment, holdings of cash and other liquid assets have, however, become increasingly costly, which has incentivised funds to reduce such holdings.[2]

The collateralisation of funds’ derivative portfolios has increased, reflecting the stricter regulatory requirements (see Chart B.1, right panel). Specifically, the European Market Infrastructure Regulation (EMIR)[3] requires the posting of two types of margin: initial and variation margin, which are to be exchanged on a daily or even intraday basis. Variation margin reflects the price movement of a portfolio of derivative contracts: if the market value of a portfolio decreases, a variation margin is called. Initial margin is an additional collateral buffer that protects a counterparty against a potential future decline in the market value of a portfolio over a short period, should the other counterparty default. For centrally cleared contracts, the exchange of both initial and variation margin is required. For non-centrally cleared contracts, the requirement to exchange variation margin was phased in in two steps and applies to all European counterparties on contracts originated after 1 March 2017. The initial margin requirements for non-centrally cleared contracts are less widespread as they continue to be phased in until September 2022.[4] Since euro area funds have around two-thirds of their portfolios non-centrally cleared, the collateralisation of their portfolios by variation margin exceeds that by initial margin. Moreover, in times of severe market stress, variation margin tend to be more procyclical and volatile than initial margin.

The size, composition and collateralisation of euro area funds’ derivative portfolios

Sources: EMIR data, sector classification from Lenoci and Letizia (2020) and authors’ calculations.Notes: Left panel: data refer to 30 March 2020. Right panel: based on selected dates close to the end of the respective quarter and the field “collateralisation” in EMIR reporting. The extent of collateralisation may be under-reported in EMIR data, owing to the limited quality of the data (e.g. missing values).

Against this background, this special feature assesses funds’ liquidity risk related to variation margin calls using two complementary approaches. It first considers the evidence on margin calls and fund liquidity drains during the recent market sell-offs in March. Second, it runs simulations of how funds may be affected in future periods of extreme stress, once their portfolios become fully collateralised by variation margin.

For both approaches, two concepts of liquidity risk are considered: sudden demand for cash in one day and demand for high-quality liquid collateral spread over several days. The rationale for the two concepts is that cash is the preferred asset class to meet an overnight or intraday call as it can be transferred between counterparties very quickly. Therefore, cash is considered as the means to cover a margin call triggered by an extreme one-day market move. In prolonged market turmoil, funds should, instead, have time to engage in collateral transformation (e.g. using repo markets) and thus a broader liquidity buffer seems relevant. It is chosen to be composed of cash and high-rated government bonds.[5] For the extreme one-day market move, it is also assumed that the timing when margin is posted and received can differ across portfolios of a fund and thus the payments cannot be netted. In the prolonged market turmoil, the exact timing is assumed to be less critical and the margin payments are netted.

The special feature uses transaction-by-transaction derivatives data collected under EMIR,[6] enriched by a sector classification[7] and liquid holdings of funds. The EMIR data are daily and cover both over-the-counter (OTC) and exchange-traded derivatives, all five main classes (i.e. commodity, equity, foreign exchange, credit and interest rate derivatives) and both centrally and non-centrally cleared trades. The data provide detailed information on both the counterparties and the characteristics of the contract, including information about (the stock of) margin posted and received. Given their large volumes and quality limitations, the data are extensively manipulated and carefully cleaned. The sector classification facilitates filtering of derivatives held by euro area investment funds and obtaining breakdowns by type of fund.

2 Margin calls on funds during the coronavirus market turmoil

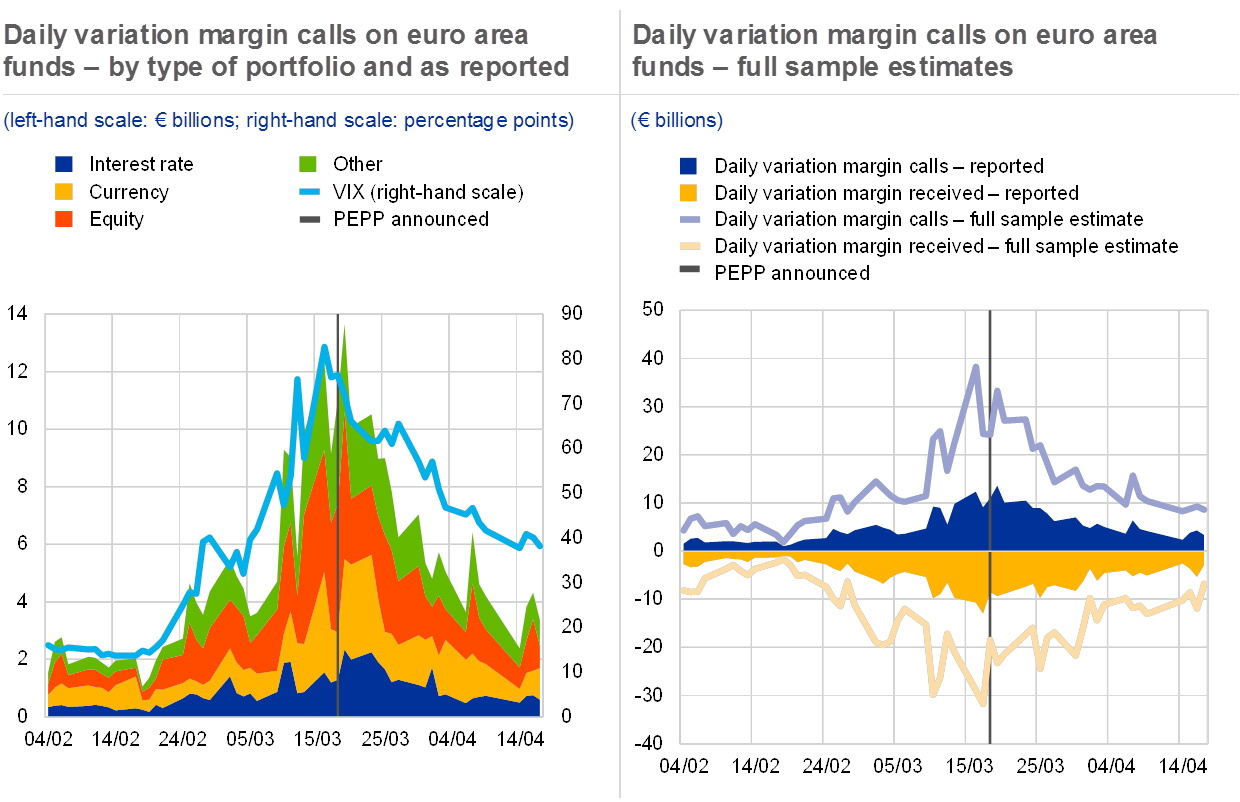

During the recent coronavirus market turmoil, the daily variation margin calls on funds’ derivative exposures rose fivefold. Based on the partial reporting of variation margin in EMIR data, the daily variation margin calls on euro area funds increased from around €2 billion in the first half of February 2020 to over €10 billion in the week beginning 16 March 2020 (see Chart B.2, left panel). The highest increase – by around 6.5 times – was reported on portfolios composed of equity derivatives, followed by interest rate (fivefold increase) and currency (fourfold increase) portfolios. The announcement of the pandemic emergency purchase programme (PEPP) on 18 March 2020 helped reduce market volatility (e.g. as measured by the VIX index for the equity market) and thus contributed significantly to the subsequent decline in margin calls.

The actual size of daily variation margin calls on funds during the turmoil could have been in the order of magnitude of several tens of billions of euro. While the exchange of daily variation margin has become a common market practice, the information in EMIR data on the size of variation margin on funds’ portfolios is often missing or not updated on a daily basis. Estimates accounting for such a gap suggest that the daily variation margin calls on euro area funds’ portfolios could have reached a daily peak of almost €40 billion on 16 March 2020 (see Chart B.2, right panel).

The size and composition of variation margin calls on funds’ derivative portfolios during the coronavirus market turmoil

Sources: EMIR data, sector classification from Lenoci and Letizia (2020), Bloomberg and authors’ calculations.Notes: Left panel: calculated as the sum of all positive margin calls on euro area investment funds, where a positive margin call occurs if either variation margin posted increases or variation margin received decreases from one day to another. The classification of derivative portfolios into asset classes is based on notional amounts using an 80% threshold: if more than 80% of the notional value of contracts in the portfolio belongs to one asset class, the portfolio is classified in this asset class. Right panel: estimates are computed by rescaling the variation margin calls proportionally to the notional amount that they represent for a specific asset class, in order to take into account the fact that some trades are reported as collateralised by variation margin (in the field “collateralisation” in EMIR reporting), but the size of the margin (in the fields “variation margin posted” and “variation margin received”) is either not reported at all or not updated on a daily basis.

Euro area funds also received variation margin during the turmoil, reflecting a mix of diverse investment strategies and different positioning within the sector. While some funds were required to post margin (blue area), others received them at the same time (yellow), so that the net margin call on the whole sector remained limited throughout most of February and March 2020 (see Chart B.2, right panel). Such netting, however, masks the individual positioning within the sector, where each fund needs to have sufficient liquidity to meet its own margin calls. Evidence from the EURIBOR futures market also suggests that the positioning of funds is relatively polarised compared with other market participants, with many funds taking either clearly “long” or clearly “short” positions in the market.[8]

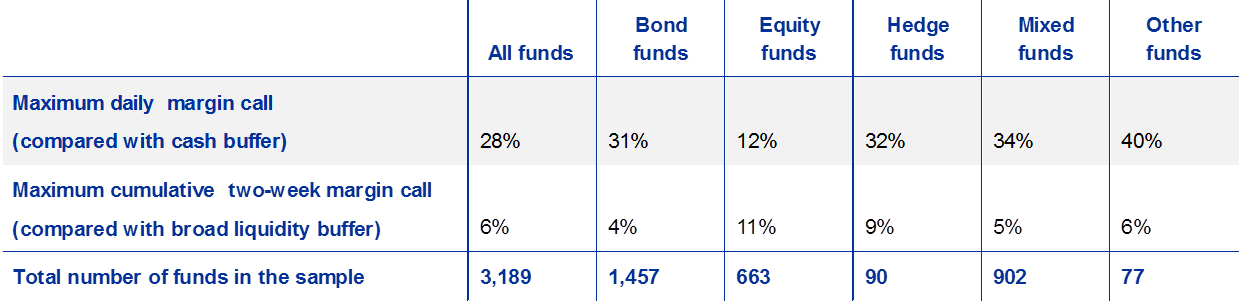

The available data indicate that a substantial share of euro area funds with derivative exposures faced a liquidity squeeze from the high margin calls. For more than a quarter of these funds, the variation margin call exceeded their pre-stress cash positions on at least one day during the turmoil (see Table B.1). In addition, the pre-stress buffer of cash and high-rated government bonds of 6% of these funds did not have a sufficient capacity to cover the cumulative two-week increase in variation margin during the market turmoil. These results should, however, be interpreted with caution as they are based on a fairly limited sample of around 3,200 funds, for which both reported variation margin calls and liquidity buffers are available. Moreover, in the high-volatility environment and taking into account the diverse positioning of funds, around half of these funds were likely to have received large liquidity inflows from variation margin calls shortly before the market turned against them.

Share of funds with variation margin calls exceeding their pre-stress liquidity position

(percentages)

Sources: EMIR data, sector classification from Lenoci and Letizia (2020), Refinitiv and authors’ calculations.Notes: The two maximum calls refer to the maximum daily variation margin call and the maximum cumulative variation margin call over a two-week period between 4 February and 17 April 2020. For daily margin calls, margin posted and received (obtained as the difference between the stock values reported in EMIR data) are not netted as the timing of payment outflows and inflows may differ. For cumulative margin calls, the exact timing is assumed to be less critical and thus the margin payments are netted. The broad liquidity buffer includes cash and holdings of high-quality government bonds, i.e. Level 1 euro-denominated bonds issued by European governments and non-euro-denominated government bonds rated at least AA.

While a substantial share of euro area funds seems to have faced liquidity strains from the high margin calls, they were generally able to meet them.[9] They could have raised cash during the turmoil by engaging in repo transactions, selling assets (e.g. money market fund shares) or drawing on credit lines. Such cash needs were beyond what might have been needed to meet other liquidity outflows during this time, for example due to redemptions (see Chapter 4), thus emphasising the potential role of investment fund margin calls in amplifying recent market dynamics. Equity and hedge funds with derivative exposures may have played a particularly important role in amplifying the downward price spirals since around 10% of them are found to have experienced liquidity strains from margin calls over a prolonged period during the market turmoil.[10]

3 Stress simulations of variation margin calls

Going forward, further extreme market shocks may occur, which calls for the conduct of forward-looking simulations of margin calls under stress scenarios. Moreover, the structural trend of increasing collateralisation of funds’ derivative portfolios is also expected to continue. Therefore, the simulations presented in this section consider two extreme stress scenarios for the three main derivative classes held by funds and assume full collateralisation of funds’ portfolios by variation margin.

To derive potential margin calls, pricing functions are developed for the ten most prevalent types of derivatives held by funds. The contracts covered include interest rate derivatives (e.g. interest rate swaps, overnight index swaps (OIS), forward rate agreements, Bund futures, and EURIBOR and LIBOR futures), equity derivatives (e.g. call/put European/American options, futures and contracts-for-difference) and FX derivatives (e.g. EUR/USD forwards). The pricing functions exploit reported contract characteristics and external data sources, and are calibrated using EMIR data.[11]

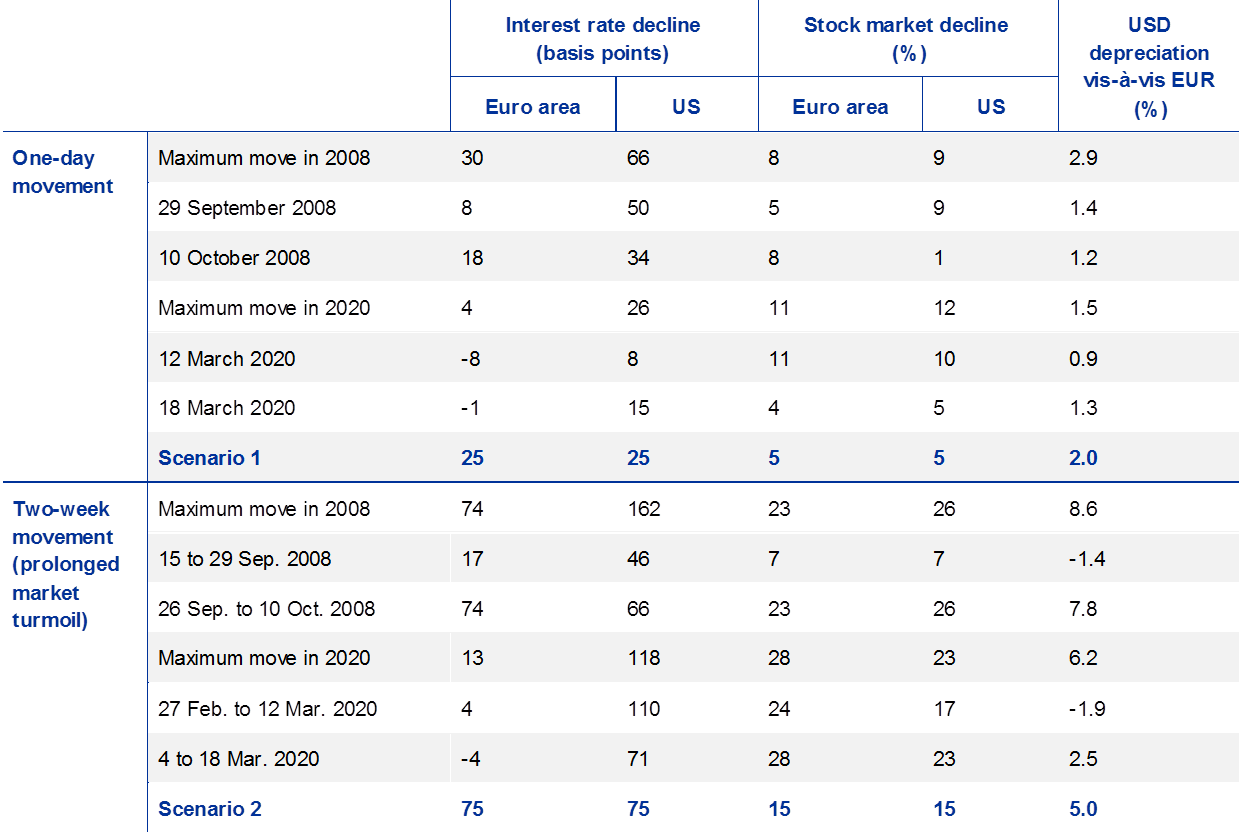

The two stress scenarios chosen are stylised and motivated by the market moves during the 2008 financial crisis and the recent coronavirus stress (see Table B.2). Specifically, the first scenario considers an extreme one-day movement, with a 25 basis point parallel downward shift in interest rates, a 5% decline in major stock market indices and a 2% depreciation of the US dollar vis-à-vis the euro. The second scenario reflects prolonged market turmoil, with a 75 basis point parallel downward shift in interest rates, a 15% decline in stock markets and a 5% depreciation of the US dollar. Although these extreme market moves did not occur as a combined shock on the same day or in the same period, they were seen separately in the three markets during the 2008 or 2020 stress episodes.

Two stress scenarios compared with extreme market movements in 2008 and 2020

Sources: Bloomberg and authors’ calculations.Notes: Interest rate declines are measured as the change in the three-month EUR-OIS and US T-bill rates for the euro area and the US respectively. Stock market declines refer to the percentage change in the EURO STOXX 600 and S&P 500 indices. Since a substantial part of euro area funds’ derivative portfolios references US markets, US figures are presented in addition to the euro area ones.

According to the simulations, 33% of funds with derivative exposures may not have sufficient cash buffers to absorb variation margin calls under the one-day stress scenario. The share is even higher for bond and “other” funds, standing at 35% and 40% respectively (see Chart B.3, left panel). The estimated cash shortfalls amount to €4.5 billion for a sample of around 3,500 funds, for which data on both derivatives and liquidity buffers are available (see Chart B.3, right panel). By rescaling the cash shortfalls to the full sample of 14,000 funds for which variation margin calls can be calculated (typically funds with sizeable derivative exposures), the overall cash shortfall is estimated to reach €31 billion. Around 53% of the variation margin call originates from equity derivatives, followed by interest rate (26%) and currency (21%) derivatives.[12]

Under the prolonged turmoil scenario, 13% of funds with derivative exposures do not have sufficient liquidity buffers to fully absorb the simulated margin call. Particularly affected are equity funds, where the share of funds with an insufficient buffer reaches 25%. This result relates to the sizeable margin calls on equity derivatives simulated in this scenario (68% of the overall call) and the relatively low holdings of high-rated government bonds by equity funds. The estimated liquidity shortfall for the limited sample of around 3,500 funds is €9.4 billion, which ‒ after rescaling to the full sample ‒ results in an estimated broader liquidity shortfall of around €76 billion.

Liquid holdings of some euro area funds are estimated to be insufficient to cover variable margin calls under two extreme stress scenarios

Sources: EMIR data, sector classification from Lenoci and Letizia (2020), Refinitiv and authors’ calculations.Notes: Based on end-2018 data. The sample with cash and liquidity buffers includes 3,523 funds, for which cash and liquidity buffers are available. The full sample includes 13,969 funds, for which EMIR data indicate a holding of a derivative portfolio and variation margin can be calculated. The rescaling to the full sample assumes that the ratio of the cash shortfall to the size of the variation margin call is the same in the two samples. It is assumed that all derivative holdings are collateralised by variation margin. The margin on funds’ portfolios is netted at the fund level only under the scenario of the prolonged market turmoil.

Conclusions

This special feature assesses the liquidity risk faced by euro area investment funds from variation margin calls on their derivative exposures. According to the simulations of extreme stress scenarios and assuming the completion of the structural move to full collateralisation by variation margin, additional liquidity needs are estimated to be around €30 billion for an extreme one-day market shock and €70 billion under prolonged market turmoil. The estimates appear realistic in view of the evidence from the recent coronavirus market turmoil, when daily variation margin calls on funds likely reached tens of billions of euro. Considering the fairly large derivative exposures of euro area funds (around €13 trillion of notional value), the estimates covering three derivative classes are also sensible when compared with the same type of simulations run on interest rate swap portfolios of European insurers[13] and pension funds (see Box A and a study by the Danish central bank[14]).

At the same time, the simulation results rely on several assumptions and, as such, have to be interpreted with caution. For example, after a shock, funds may rebalance their portfolio, but the analysis assumes that portfolios are static.[15] In addition, the cash/liquidity buffers considered are relatively narrow as funds may have the option to use less liquid assets to cover margin calls. Moreover, the analysis assumes that the move towards full collateralisation of funds’ portfolios by variation margin calls has been completed. On the other hand, investment funds’ liquidity needs would be aggravated if margin calls were combined with redemption requests and/or falls in prices of assets used as collateral such as in the recent market turmoil. Recent events have also highlighted how a combination of liquidity risks in investment funds can play a key role in amplifying adverse market dynamics.

The results call for the development of macroprudential tools to address the liquidity risk in the fund sector as this risk can have wider systemic implications. Such tools should focus on containing the build-up of vulnerabilities before risks materialise. Regulatory requirements aimed at strengthening funds’ ability under stress to meet potential funding needs, including variation margin calls, could be effective in this respect. Such tools would make the sector more resilient to future financial turbulence and decrease the need for ex-post interventions (see Chapter 5).

Box ALiquidity stress simulations of euro area pension funds’ interest rate swap portfolios

Euro area pension funds are currently exempted from the central clearing obligation under EMIR, and may continue to be exempt until 18 June 2023.[16] The exemption means an important category of active derivatives users are currently left out of the scope of the central clearing obligation. The primary reason behind this exemption is that without it, pension funds could face an increase in liquidity risk as they would be required to adhere to risk management of central counterparties (CCPs), including the daily exchange of variation margin (VM) in cash, which they may not currently hold in sufficient amounts.[17] In response, pension funds could increase their cash holdings, which would, however, adversely affect their investment returns, which are already under pressure in the low-yield environment (see also Chapter 4 on the profitability challenges of life insurers, which are similar to those faced by pension funds). Alternatively, they could rely on other solutions such as market-based collateral transformation to convert their bond holdings into cash when needed.

Against this background, this box assesses the liquidity risk faced by pension funds from transitioning to central clearing. The analysis focuses on Dutch pension funds as they provide a good proxy for the euro area pension fund sector: at the end of March 2020, they accounted for 80% of the derivatives of all euro area pension funds.[18] In addition, the analysis is targeted at interest rate swaps, which are mandated for central clearing and where the share of Dutch pension funds is even higher, standing at 89%.[19]

Pension funds use interest rate swaps to hedge the interest rate risk arising from their long-dated liabilities whose duration exceeds that of their assets. Therefore, an increase in interest rates would trigger CCP VM calls on pension funds’ interest rate swap portfolios. To simulate such VM calls, an extreme one-day +100 basis point parallel shift in the yield curve is assumed.[20] While the size of the shock may be extreme, it is commonly used as a baseline stress scenario by the industry.[21] To simulate the impact, the analysis uses fund-by-fund supervisory data from De Nederlandsche Bank (DNB) on liquidity buffers and derivative exposures, complemented by EMIR data. In the analysis, the liquidity buffers and the hedging profiles are assumed to be static.

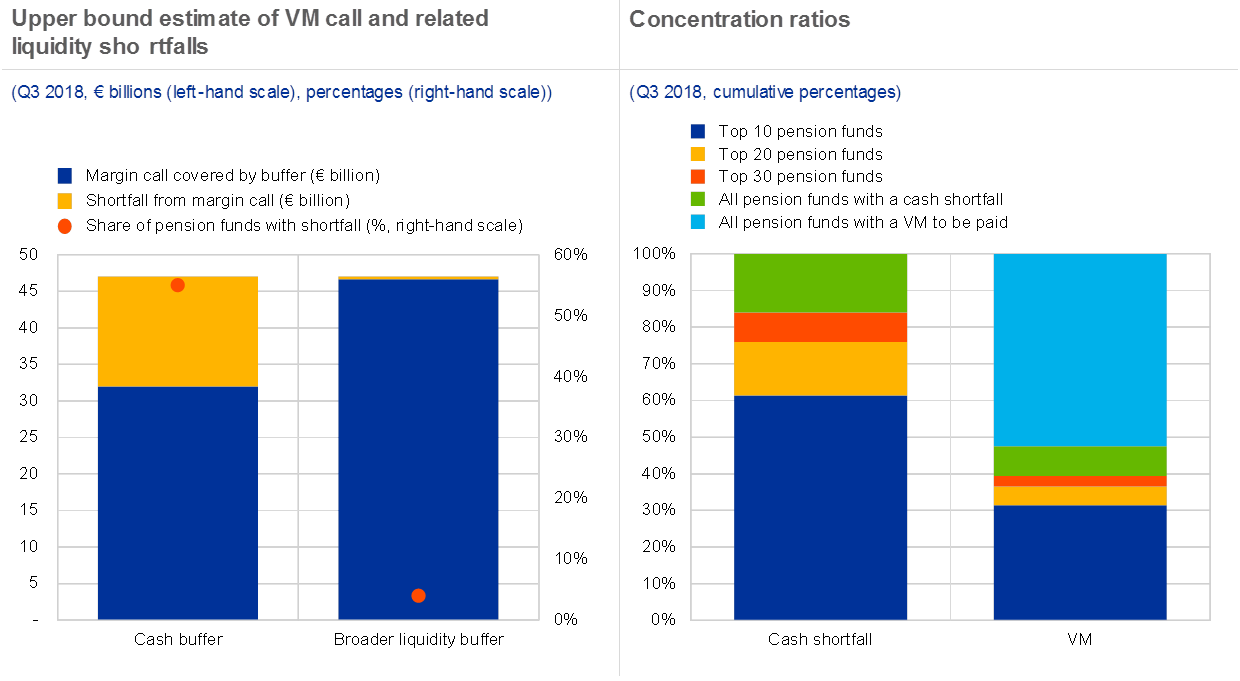

Chart A

Results of a stress scenario of a +100 basis point parallel shift in the yield curve

Sources: DNB data as reported by pension funds and authors’ calculations.Notes: The sample includes 187 pension funds. Cash buffer includes freely disposable cash and reverse repos. Broader liquidity buffer includes cash buffer and AAA- and AA-rated government bonds of advanced economies. The ranking (top 10, 20 and 30) is based on the size of cash shortfalls.

Under the simulated stress scenario, VM calls on interest rate swaps held by Dutch pension funds could be between €36 billion and €47 billion, resulting in an aggregate cash shortfall of €6 billion to €15 billion. Using the upper bound estimate of the aggregate cash shortfall of €15 billion, around 55% of Dutch pension funds would not have sufficient cash to cover their VM calls (see Chart A, left panel). The cash shortfalls would be concentrated within a small number of pension funds with relatively low VM payments (see Chart A, right panel). For instance, 61% of the overall cash shortfall is attributed to ten pension funds, which have a share in VM payments of 32%.

The analysis shows a potential €15 billion cash shortfall and 96% of Dutch pension funds are found to have a sufficient amount of high-rated government bonds that could be used for collateral transformation. For the remaining 4%, the lack of high-rated government bonds is very low, at below €0.35 billion. Assuming that pension funds source funding via market-based collateral transformation, the cash shortfall can be considered contained when compared with the overall size of the repo market. The results underline the importance of pension funds’ individual preparedness to use market-based collateral transformation or other options to fund their stressed VM calls, when needed.

- [1]Audrius Jukonis and Elisa Letizia worked on this article while being affiliated with the ECB. Francesca Lenoci provided valuable data support.

- [2]See, for example, Financial Stability Review, ECB, November 2019.

- [3]Regulation (EU) No 648/2012 of the European Parliament and of the Council of 4 July 2012 on OTC derivatives, central counterparties and trade repositories (OJ L 201, 27.7.2012, p. 1).

- [4]For the details of risk-mitigation techniques applicable to non-centrally cleared derivatives, see Article 11 of EMIR and the related Commission Delegated Regulation (EU) 2016/2251 of 4 October 2016 supplementing Regulation (EU) No 648/2012 of the European Parliament and of the Council on OTC derivatives, central counterparties and trade repositories with regard to regulatory technical standards for risk-mitigation techniques for OTC derivative contracts not cleared by a central counterparty (OJ L 340, 15.12.2016, p. 9). On 3 April 2020, the deadlines for completing the final two implementation phases of the margin requirements were extended by one year (see this press release).

- [5]High-rated equities are not included in the broad liquidity buffer as they may quickly turn illiquid and lose value in severe market distress such as the recent coronavirus turmoil. The size of the repo market for equities is also limited and the haircuts applied in this market are high.

- [6]While the reporting obligation applies to all EU-located entities that enter into a derivatives contract, this special feature is based on a sub-set of the data, to which the ECB has access. In most cases, these data are reported by euro area counterparties. See Article 2 of Commission Delegated Regulation (EU) No 151/2013 of 19 December 2012 supplementing Regulation (EU) No 648/2012 of the European Parliament and of the Council on OTC derivatives, central counterparties and trade repositories, with regard to regulatory technical standards specifying the data to be published and made available by trade repositories and operational standards for aggregating, comparing and accessing the data (OJ L 52, 23.2.2013, p. 33).

- [7]Lenoci, F. and Letizia, E., “Classifying the counterparty sector in EMIR data”, ECB Working Paper, forthcoming.

- [8]See Boneva, L., Böninghausen, B., Fache Rousová, L. and Letizia, E., “Derivatives transactions data and their use in central bank analysis”, Economic Bulletin, Issue 6, ECB, 2019.

- [9]A US client of ABN Amro Clearing bank, presumably a volatility-focused hedge fund, is one reported case of a failure to meet the margin requirements in the extreme stress situation (see this risk.net article).

- [10]Recent studies by the Bank of England and the Bank for International Settlements (BIS) emphasise the role of variation margin calls on non-banks in amplifying market dynamics in the UK and US markets respectively (see Schrimpf, A., Shin, H. S. and Sushko, V., “Leverage and margin spirals in fixed income markets during the Covid-19 crisis”, BIS Bulletin No 2, April 2020; and, “Interim Financial Stability Report”, Bank of England, May 2020). In particular, the BIS study points out that (leveraged) hedge funds involved in relative value strategies were unable to meet variation margin calls on their US Treasury futures and their positions were unwound by dealers/exchanges, which further exacerbated the Treasury price declines.

- [11]Missing contract characteristics (e.g. starting dates, frequency of payments, etc.) are set to most common market practice. Current and historical prices of underlying instruments that are necessary to price plain-vanilla contracts (e.g. yield curves in different currencies, equity indices and stock prices, exchange rates) are sourced from external data providers. Whenever possible, reported market prices (e.g. fixed interest rates, exchange rates, futures prices) are matched to the end-of-day mid-prices and inconsistent or missing values are either transformed, dropped or replaced. Volatility parameters for contracts that involve optionality are calibrated directly to the EMIR data to obtain a smooth volatility surface using a sequential resampling algorithm that exploits the large scale of the data. For more details, see Jukonis, A., “EPIC: an EMIR based derivative pricing and stress testing tool”, unpublished manuscript, 2019.

- [12]This result emphasises the importance of moving beyond the analysis of only interest rate derivatives, which have been the focus of the few existing studies on this topic so far. See, for example, Financial Stability Report, Bank of England, 2018; Bardoscia, M., Bianconi, G. and Ferrara, G., “Multiplex network analysis of the UK OTC derivatives market”, Staff Working Paper No 726, Bank of England, 2019; Bardoscia, M., Ferrara, G., Vause, N. and Yoganayagam, M., “Simulating liquidity stress in the derivatives market”, Staff Working Paper No 838, Bank of England, 2019; and Glasserman, P. and Wu, Q., “Persistence and procyclicality in margin requirements”, Management Science, Vol. 64, 2018.

- [13]De Jong, A., Draghiciu, A., Fache Rousová, L., Fontana, A. and Letizia, E., “Impact of variation margining on EU insurers’ liquidity: an analysis of interest rate swaps positions”, Financial Stability Report, European Insurance and Occupational Pensions Authority, December 2019.

- [14]See “Pension companies will have large liquidity needs if interest rates rise”, Danmarks Nationalbank, November 2019.

- [15]In view of the elevated market volatility since March 2020, some market participants put in place temporary restrictions on the trading of certain contracts (see this FT article).

- [16]See Regulation (EU) 2019/834 of the European Parliament and of the Council of 20 May 2019 amending Regulation (EU) No 648/2012 as regards the clearing obligation, the suspension of the clearing obligation, the reporting requirements, the risk-mitigation techniques for OTC derivative contracts not cleared by a central counterparty, the registration and supervision of trade repositories and the requirements for trade repositories (OJ L 141, 28.5.2019, p. 42).

- [17]Central clearing may be used as a clearing member or as a client. Should pension funds use central clearing as clients, they may be provided with collateral transformation by their intermediating clearing members, which, in turn, would reduce the need for pension funds to post VM in cash.

- [18]In terms of the notional amount and according to EMIR data.

- [19]While pension funds also heavily use FX derivatives, these contracts are currently not subject to mandated clearing. Thus, for the purpose of assessing the liquidity shortfalls, the interest rate swap portfolios are studied in isolation in view of the Eurosystem’s contribution to the discussions on the impact of the central clearing obligation on pension funds.

- [20]While this shock is negative for the value of pension funds’ interest rate swap positions and thus poses liquidity risks, it is positive for the overall financial position of pension funds.

- [21]For instance, the study prepared by Europe Economics and Bourse Consult for the European Commission also applies this stress scenario.